FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro : EUR/NZD slips lower after soft US jobs report

FxWirePro : EUR/NZD slips lower after soft US jobs report  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: AUD/USD eases as investors await U.S. employment figures

FxWirePro: AUD/USD eases as investors await U.S. employment figures  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data

FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

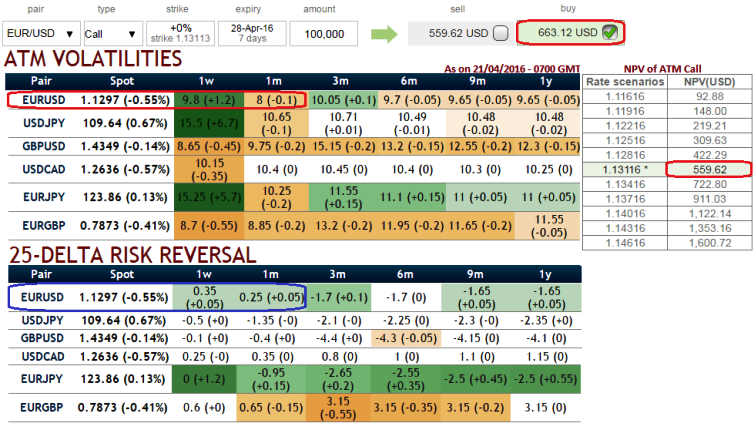

At spot FX flashes of EURUSD at 1.1302 we see delta risk reversal for contracts of 1W and 1M expiries have shown bullish recovery signals, but in long term (3M-1Y) put contracts are on higher demand.

But the participants seems to have shrugged off the bullish hedging sentiments in EURUSD OTC FX markets as you can make out from the nutshell showing EURUSD’s implied volatilities of 1M at the money contracts are shrinking away, the least among G7 currency space, almost at 8%.

As a reminder, this feeble IV represents no much movement in underlying FX market could be expected from EURUSD during the life span of the option.

In that respect, an option buyer is partially buying the market's expectations for this pair.

Contemplating these factors and synthesizing while projecting the trend, how do you want to stay long but worried about sluggish IVs in OTC FX markets that are not substantiating overpriced premiums:

1W ATM IVs of this pair are at 9.8% and the premium on 1W call are trading 18.4% more than Net Present Value, hence it is deemed as a huge disparity between option prices and volatilities in FX option markets.

A synthetic long call is created when underlying spot FX position is combined with a long put of the same series.

It is so termed because the established position has the same profit potential as a long call. Profitability through this strategy would be unlimited as same as naked calls, maximum risk would be to the extent of initial premium paid to play the role of put holder.