China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

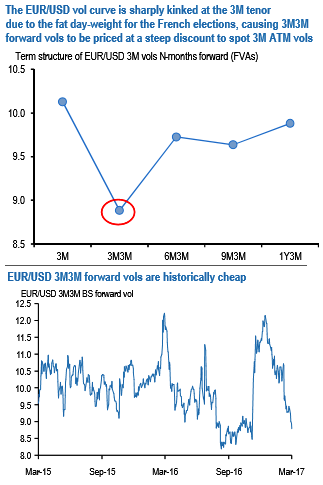

The European election-distorted EUR/EUR-cross vol curves: The risk premium for the French elections has distorted EUR-and EUR-cross vol surfaces. 3M-1M vol curves have steepened enormously due to the boost to 3M expiries from the fat day-weight associated with the second round vote on May 7th; post-3M vol curve segments are inverted however as the event effect fades in longer tenors (refer above chart).

The inversion of the 6M-3M segment and the resulting steep discount of 3M3M forward volatility (FVAs) to 3M ATMs has sparked interest in buying EURUSD 3M3M FVAs as an asymmetric election hedge at levels that appear historically favorable, especially after the sharp sell-off in vols this week (refer above chart).

It seems instinctive enough that 3M3M forward vol should deliver substantial positive returns in the event of an unexpected Le Penn victory, yet the dynamics of implied vols around a binary event can be a little murky since the shock of a tail outcome intersects with the offsetting effect of implied vols collapsing as a large day-weight rolls off the option expiry window (note: no such conflict with realized vols/gamma which explode when spot reacts violently to a shock result). Where this tension eventually re-sets implied vols after the event is difficult to quantify ex-ante, but we can at least look back at the two major political disruptions last year to judge how much merit there was in buying FVAs.

We examine the performance of 3M3M FVAs in GBPUSD around the Brexit referendum and USDMXN around the US elections initiated 2-months prior to event dates, roughly the time-to-event in the current instance. Initial conditions in terms of vol levels and curve slopes are not strictly comparable across episodes, but the consistency of outcomes across the (grand sample size of) two episodes is comforting.

Two key takeaways from chart 6 are: (a) in both cases, FVAs delivered 2.3-2.8 vols of peak P/L on mids and are able to monetize nearly the entire ex-ante static slide along the term structure, meaning that ATM vols do not roll down at all after a left tail outcome despite the passage of event risk; and (b) optimal entry timing into FVAs is 4-5 weeks before D-day when the pricing of event.