UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

The steeper EUR vol curve on ECB’s soft taper As has become par for the course in recent years, the December ECB meeting surprised by delivering a soft taper that reduced the pace of asset purchases, but forestalled a vicious bond market rout by offering a maturity extension sweetener and keeping open the possibility of increasing program size/duration as required.

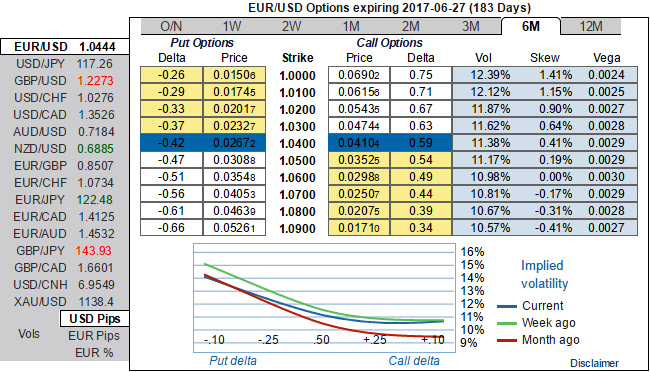

Both Short and longer term volatilities are likely to benefit the USD - Diverging monetary policy indicate a stronger USD. While risk reversals of 6m tenors also indicate the high degree of bearish risks. 6m IV skews are the evidence of the hedgers’ interests of OTM put bids.

Longer-dated implied vols, especially expiries spanning the Dutch and French elections should, however, prove to be a more reliable, persistent store of event risk premium and relatively immune to tactical gamma developments.

As a result, in the diagram, please note and compare yield curves (2:1 PRBS) on shorts (of 1m expiry and 6m expiry) in put ratio back spreads, when you deploy shorter tenor in option writing, the chances of obligation would be lesser as you could see the similar strike on 1m expiry carries attractive positive cashflows than on 6m expiry because of less chance of exercising options.

List of major significant events in H1’2017 that could pose potential risks to EURUSD and 6m OTC indications to address these events:

As was widely expected, the FOMC raised the target range for the federal funds rate by 25bp to 50-75bp at its December meeting.

On the flip side, the FOMC is likely to raise its target range for Fed Funds interest rates by 25bp to 0.50%-0.75%, almost exactly one year after the first rate step that brought an end to zero pct interest rates.

Although the road to the first round of the French Presidential election (23 April) is still long, we believe Mr Fillon’s election as the Republicans’ candidate should provide the markets with some reassurance. Under our baseline scenario, we see a referendum on EU/euro membership as unlikely. Such a referendum remains highly dependent on the results of the general election.

Italy remained in the spotlight this week with a new government, mixed news about banking sector restructuring and risks of a referendum on past labor market reform.

Elsewhere, the upcoming German federal polls would elect the members of the Bundestag, the federal parliament of Germany in 2017.

The expectation of EURUSD to reach parity between now and the French elections in April/May. For the Euro, this hawkish surprise comes a few months ahead of our expected timeline, and should partially offset the dollar drama unfolding since last month’s US Presidential elections as well as any low-intensity European electoral stress next year to restrict EURUSD to a fairly tight 1.04 – 1.08 range over coming months.