Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

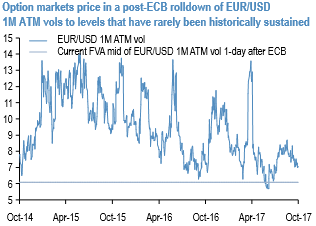

Let’s have a glance through volatility surface in euro crosses before we begin with this write up, 1m EURUSD ATM IVs have been the least among the G7 FX space. IVs of all euro pairs have been considerably shrinking away despite lingering geopolitical issues.

That sinking feeling: Implied and realized volatilities across Europe continue to sink steadily with short-term realized volatility on European indices having touched their lowest ever levels this month (20-day vol below 5%). In this note, we try and explain some drivers of these moves.

Extreme low sector correlation is accelerating the process: One other key market metric at all-time lows is the average pair-wise correlation between sector prices. We break-down the index vol into single stock vol and correlation components (as measured in dispersion). We find evidence that the dispersion of returns between is a key driver of the recent weakness of European index vols. However, it’s also evident that index vol itself is under pressure.

Evidence of gamma saturation from hedging: On most European indices, we find that close-to-close vol has been significantly lower than realized vol calculated on an intraday basis since Q4-2016 – a period that we believe has coincided with the higher selling of vol risk premium. An obvious reason is the hedging flow from market makers (generally done at the close). This is definitive proof of this oft-mentioned large positive gamma positioning and of its impact on vol.

Visualizing the low vol trap: Lower volatility makes the gamma exposure of hedging accounts higher – simply because gamma is defined as the change in delta for a 1% move in the spot. We present simple charts to quantify the effect and explain how it contributes to the low vol trap. We also suggest how to position in such an environment, citing a few examples.

What’s needed to change the situation? Among the two drivers discussed in this note, the extremely low sector correlation seems to be the more temporary one. It’s hard to imagine a 1-month sector correlation below 10% for more than a few weeks. Gamma saturation or the low vol trap, on the other hand, is trickier. Only a real change in the economic environment and fall in profit trends would reduce the pre-eminence of the short vol trade.