Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

EUR was the best performing major last year (+13% vs USD, +8% on the NEER) as a substantial upswing in the business cycle intersected with a downshift in the political risk cycle. EUR became economically and politically investable and the resultant inflow of long-term investment capital lifted the surplus on the region’s basic balance to its strongest ever level (€500bn).

This inflow allowed the currency to close the valuation gap that had been established as a consequence of ECB policy and political risk (the EUR REER was 9% cheaper than its 20Y average ahead of the French election).

We could foresee EUR to continue its rehabilitation this year. The region’s economy is expected to outpace the US for the third consecutive year notwithstanding US tax cuts; the ECB will end QE as a prelude to tightening in 2019.

EUR bond yields should rise by more than in other DM countries as they are more overvalued; balance of payments trends should remain strong and counter a further deterioration in front-end rate differentials; and political risks should be laid to rest for the next 1-1/2 years if Italy elects a mainstream government as seems probable based on the trend in the opinion polls (we attach only a 5% probability to a non-mainstream government.

On the flip side, JPY underperformance has been the highlight as well as USD softness. Consequently, USDJPY remained in a roughly three yen range while yen’s NEER marked the lowest level since February 2016 on January 5 this year though it has rebounded this week. Meanwhile, JPY crosses extended the upside; EURJPY reached 136-handle for the first time in more than two years.

For now, EUR optimism is more safely expressed through EURJPY, this pair is a safer vehicle to position for stronger European growth and the risks that this could persuade the ECB to dispense with an additional taper and end QE already in September.

EURJPY PPP and FEER valuations are the yen bear’s arch-enemies, but they apply far more to the USDJPY than to the EURJPY, given that the euro, too, is significantly undervalued on a PPP basis. The PIIE puts a FEER-consistent EURJPY rate at 121. More important perhaps than the valuations, however, is our confidence that the ECB is further along the road to policy normalization than the BOJ.

As stated in our previous write up on the technical trend of this pair, the consolidation phase of EURJPY has remained intact.

While EURJPY risks reversals have been indicating bearish risks, and the positively skewed IVs have also been substantiating the similar bearish stances.

Hence, coupled with all fundamental, technical factors and OTC indications, it is advisable to initiate below relative value trades.

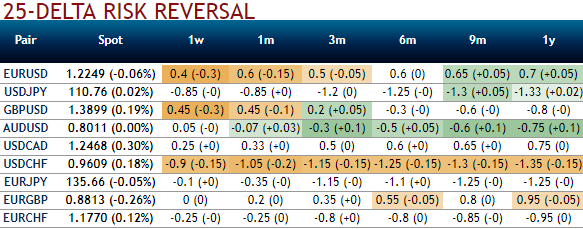

Sell 6M EURJPY 25D risk-reversal (buy EUR calls - sell EUR puts), delta-hedged for risk-averse traders.

Buy 3M EUR puts/JPY calls vs. sell 3M 28D EUR puts/KRW calls for directional traders.

Buy 3m EURJPY ATM -0.49 delta puts for aggressive bears on hedging grounds. Courtesy: SG JPM

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards 32 levels (which is bullish), while hourly JPY spot index was at -155 (mildly bearish) while articulating (at 07:32 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: