China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Euro area GDP is expected to pick up in the final quarter of 2016. The underlying price pressures remain weak, but the latest economic data demonstrates that economic growth has remained moderate. Q3 GDP growth was 0.3% QoQ, the same as the prior quarter, and survey indications suggest that it will be stronger in Q4.

But the main risks events are now in the euro zone (ECB ahead in 2017, post-Brexit formalities and immigration tensions).

On long-term perspectives, the security and political risks should weigh on the EUR:

There also remains the prospect of further easing measures from the ECB (for example a formal extension of QE beyond March 2017).

The political risks are clouded in the euro area. The euro area economy has so far weathered political surprises in the form of the UK’s referendum vote to leave the EU and the election of Donald Trump as the next US President.

Euro-area political indecisions would now be prevalent over the coming year, with key elections taking place in –

The Netherlands (15 March),

France (first round of the presidential election on 23 April and second round, if necessary, on 7 May) and

Germany (by 22 October).

Latest polls advise that the far-right Freedom Party may win the most seats in the Netherlands, although without a majority.

In France, the far-right candidate Le Pen is expected by commentators to make it to, but not win, the second round. An unexpected victory for Le Pen would call into question the EU project.

In Germany, the Chancellor Merkel is expected a victory for the fourth term, although the right-wing AfD party is a key wildcard.

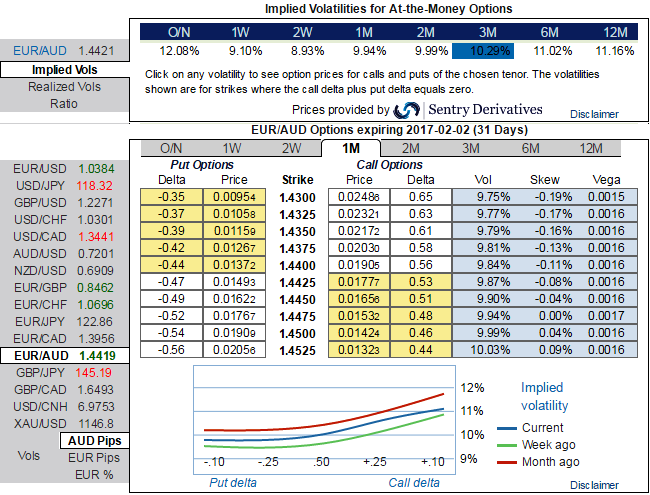

OTC Outlook and Hedging Strategy: EUR/AUD

As you can probably guess from the positively skewed IVs in 1m tenors lures ITM put option writers’ opportunities. An option writer wants lower IV or IVs to shrink away so that the premium would also drop accordingly which could be the conducive case here if we have to evaluate OTC tools. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

Subsequently, 2m implied volatilities are considerably spiking on higher side that is most likely to favor vega puts in the robust downtrend.

As a result, we believe in jacking up in long leg of the below option strategy:

Initiate longs of 2 lots of 2m at the money vega put options, simultaneously, short 1 lot of (1%) in the money put of 2w expiry with positive theta. It is advisable to prefer European style options.