FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro: USD/ZAR gains some ground, but downtrend remains

FxWirePro: USD/ZAR gains some ground, but downtrend remains  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report

FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)

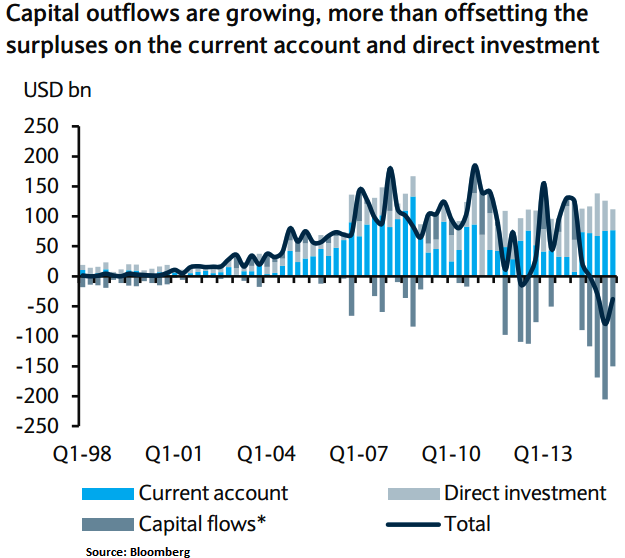

Although China's capital account is closed, several illicit channels of capital outflows have made the capital account rather leaky. Leaky capital account estimates outflows and policy implications, the capital outflows from China could rise from the current 8-10% of GDP, driven by slowing growth, financial market volatility, policy uncertainty and currency overvaluation. In an adverse scenario, total outflows on the capital account could rise to a significant - 15% of GDP. Since these outflows are much larger than current account inflows of 5% of GDP, they will pressure China's FX reserves and/or the CNY exchange rate.

The valuation models from Barclays, it suggests that the CNY is about 5-10% overvalued and with China's growth prospects deteriorating, if China absorbs the balance of these outflows (USD1trn) completely by selling reserves and meeting hedging demand (in forward markets), this implies a drawdown of 28% of the current reserve portfolio. We believe this is a significant amount, especially if authorities are unable to slow capital outflows. We expect a weaker CNY over the medium term and significant jump risk for USDCNY as sustained intervention of such a size is unlikely given the uncertainty of success.

We see risks of capital outflows and CNY depreciation pressure persisting. We think a 10% fall in the CNY versus the USD is needed to stabilize the REER and capital outflows. It is recommended a long USDCNH 6-month forward trade and maintain our USDCNH call spread.

Forecasts (USD/CNY)

Spot - 6.37, Q4'15 - 6.80, Q1'16 - 6.90, Q2'16 - 6.95, Q3'16 - 7.00

Outright Forward

Q4'15 - 5.4%, Q1'16 - 6.0%, Q2'16 - 6.2%, Q3'15 - 6.3%.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Extended impact of CNY on capital outflow – USD/CNY trade strategies

Tuesday, September 22, 2015 12:13 PM UTC

Editor's Picks

- Market Data

Most Popular