Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

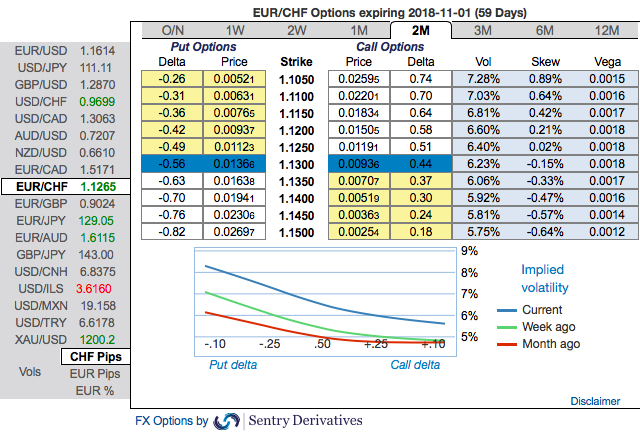

The EURCHF exchange rate has already eased back below the 1.13 mark and has therefore returned into areas that are likely to begin causing the Swiss National Bank (SNB) discomfort.

The central bank had seemed much more relaxed as regards the exchange rate when it climbed from levels around 1.10 to above 1.14 last year. Even though inflation in Switzerland is positive again, core inflation has remained at only 0.5% since the start of the year, which is anything but comfortable.

As a result, we would assume that the SNB will still not like to see strong franc appreciation. There is an acute risk of the SNB intervening the closer the EURCHF exchange rate gets to the 1.10 mark.

We maintain a decent exposure to CHF this week but rotate a slightly underwater position in USDCHF into an outright short in EURCHF due to ongoing noise in Turkey and what could be a greater focus by investors on the Italian budget into September.

GBPCHF has performed very well as investors for whatever reason have belatedly woken up to the non-negligible risk of a no-deal Brexit, and the sensitivity of GBP to this would suggest that investors have some reasonable GBP exposures that are under hedged.

As for CHF itself, we continue to highlight the ever-present positive balance of payments disequilibrium that can only be exacerbated by heightened EM stress, namely a current account that is too large for private sector investors to recycle given still relatively low average rate differentials between CHF and ROW.

The SNB has pretty much single-handedly recycled this surplus for an entire decade since the GFC hit, but with a balance sheet that has mushroomed to 125% of GDP as a result of this systematic FX intervention, legitimate questions marks exist over the SNB’s capacity and willingness to continue to take the other side of commercial flows, let alone absorb another round of deleveraging of whatever cross- border CHF funding positions may exist.

It is quite notable that the SNB appears not to have intervened since EURCHF rejected 1.20 back in early May.

Short in EURCHF at 1.1265, stop at 1.1350.

EURCHF risk reversal numbers and positively skewed of implied volatilities of 2m tenors signify mounting risks. Accordingly, we advocate 2m (1%) in the money -0.79 delta put options, the rationale for choosing such derivative instrument is that the deep in the money call with a very strong delta would move in tandem with the underlying move.

Stay short GBPCHF from 1.3051. Marked at 2.29%. Lower stop to 1.30.

Buy 6M GBPCHF - GBPUSD vol spread, equal-vega notional. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly EUR spot index has shown 5 (which is neutral), while hourly CHF spot index was at 84 (bullish), while articulating at 12:22 GMT. For more details on the index, please refer below weblink: