Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

The British economy advanced 0.5 pct on quarter in the three months to September of 2016, slowing from a 0.7 pct expansion in the previous period and in line with the preliminary estimate. Net external demand was the main driver of growth, while household expenditure and fixed investment rose at a slower pace.

But GDP forecast for 2017 has been revised up to 1.0% and remove our call of a rate cut early next year. Rather, we expect the BoE to remain on hold over the forecast horizon.

We also highlight that trend growth has decreased in recent years to about 1.5% today. Brexit, if anything, poses downside risks to this estimate.

Inflation and retail sales data released this week came in on the strong side, while the labor market report showed that employment fell and claimants increased.

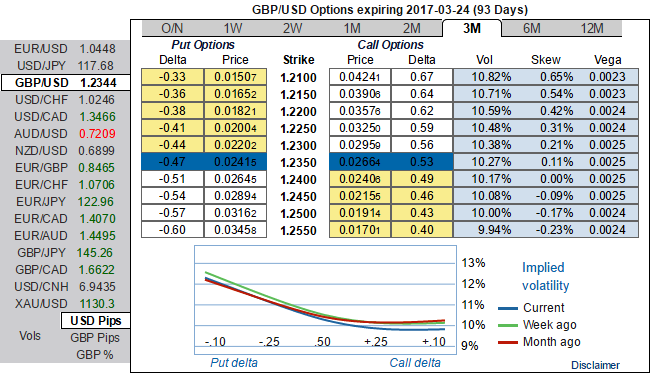

The discounted gloomy UK outlook both prevents a new bold depreciation and a much stronger currency. The technical picture suggests a new turbulence and bearish pressures.

Owing to the above fundamental factors, GBP vols and risk reversals have been unchanged but to remain negative flashes to mitigate bearish risks in long run, while IV skews are also bidding OTM put strike which is line with the risk reversal indications.