Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

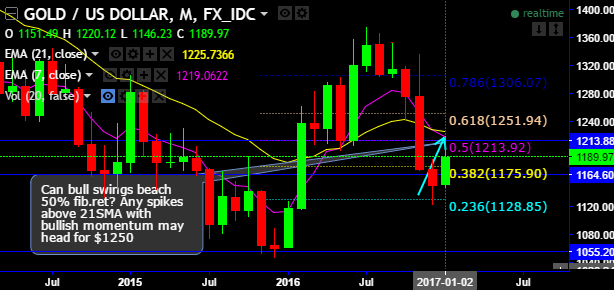

Gold prices in January series have retraced back above 38.2% Fibonacci retracements from the lows of six months downtrend (i.e. 1122.81 levels), earlier the upswings have hit 50% but could not sustain to slide to the current 1190 levels.

OTC outlook:

The current implied volatility of 1m ATM XAUUSD contracts are at 12.45% and above with positive skews signifying hedgers interests are in well balanced on either side but slightly biased towards OTM call strikes, and it is likely to spike higher for 1m tenors.

While delta risk reversals substantiate these figures with upside risk sentiments (observe positive shifts across different tenors). By this, we mean guaranteed hedge at the higher strike (worse than the outright forward rate if unleveraged) in order to benefit from a favorable market move down to the lower strike.

US yields have retreated off their mid-December highs and gold prices have simultaneously increased more than 5%. Given the looming, largely uncertain, catalyst of the US inauguration and the launching of the first 100 days of Trump’s presidency, we decided to lock in our gains and close our position at today’s settlement price of $1,196.60/oz for a gain of 6%.

Although the major trend has been puzzling, the moment in short-term upswings is intensified while six months downtrend can also not be disregarded, accordingly, we’ve formulated below hedging strategy using option contracts.

Hedging Strategy: Option straps (XAU/USD)

As the risk reversal numbers allow for a customized hedging solution, tailored to your risk and hedging profile contemplating both side risks. Risk Reversals are OTC derivative instruments and the notional amount does not need to be tied up throughout the full tenor of the trade.

Hence, we recommend deploying hedging strategies to arrest upside risks with longs positions in 2 lots of ATM vega calls with 1M expiry and 1 lot of ATM vega puts of similar expiries.

Vega instruments are preferred as it takes care of the sensitivity of an option’s value to a change in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.

As shown in the diagram, the Vega of a long call option position is USD138 and IV increases or decreases by 1%, the option’s premium will increase or decrease by USD138, respectively.

Subsequently, this XAUUSD option straps strategy would take care of ongoing upswings and abrupt downswings and yields handsome returns.