Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

The Federal Reserve offered up a clearly hawkish monetary policy - confounding market's skepticism and staging the Dollar

Risk trends are perhaps at greatest risk of volatility moving forward post-Fed QE plans, but it may take time to register.

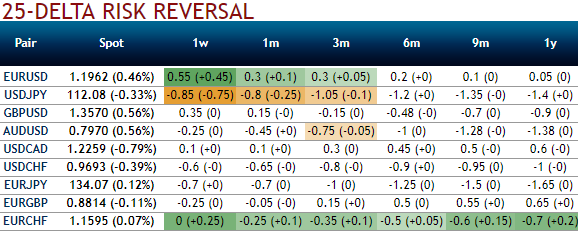

For an instance, the USDJPY 1m risk reversals scale is still near to a 3m high of -0.85 (currently at -0.80), suggesting falling demand for downside bets, i.e. put options.

25-delta risk reversals show the difference in volatility between puts and calls. A positive number indicates upside protection on the underlying forex spot [calls] is relatively more expensive. A negative number indicates puts are more expensive than calls.

The improvement in the risk reversals adds credence to the solid rally in the USDJPY spot and the Treasury yields.

Long gamma, flat/selectively short vega is the appropriate ex-ante vol portfolio orientation if we are correct on flow dynamics.

The other noticeable development on option surfaces as a result of Q3’s dollar bear trend has been the sharp compression of risk-reversals (refer 1st chart) as realized spot-vol correlations ran counter to their usual positive directionality. It will be a stretch to claim that a V-shaped rebound is in the pipeline if the dollar pauses, since USD riskies did not deliver even during the dollar bull run of 2014-16 outside of select and short-lived market shocks, but it does not stretch the imagination to consider at least a local trough in USD-skews around current levels if markets are entering a period of consolidation.

If we are correct on the pressure on mid-curve vol from partial unwinds of bearish dollar options and a temporary base in risk-reversals, overwriting 3M expiry OTM USD puts on cash dollar shorts is one way of reducing bearish USD exposure while still retaining partial exposure to the theme and collecting some handy premium in the process. Indeed, 2nd charts and 3rd chart show that USD put overwriting has been a useful risk-reduction strategy for short dollar portfolios over time, even if they have not necessarily proven to be return enhancers in the mold of equity calls.

USD put overwritten short dollar portfolios experience an improvement in average return/drawdown ratios of between 50% -100% vis-à-vis cash dollar shorts depending on the currency universe, with benefits most acute for EM FX that are most equity-like in terms of vol risk premium, and where the heavy hand of central bank intervention often constrains runaway currency appreciation.

At current prices, USD puts/G10 calls ex-GBP and JPY are relatively more expensive compared to USD puts/EM calls largely due to the run up in EURUSD and EUR-bloc vols over the past two months, and accordingly are the best overlays for a short dollar portfolio. Courtesy: JPM