China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

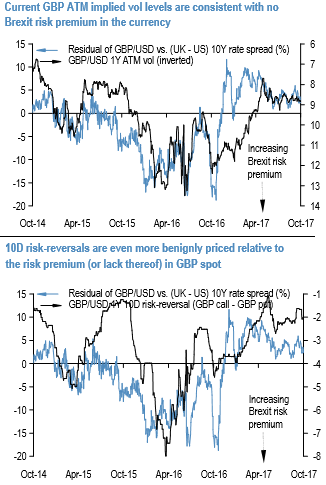

GBP has been a currency with substantial fundamental uncertainty for now in our view. One side Brexit transition and on the other hand, the abrupt change in the BoE’s reaction function triggered a sharp GBP rally in September. However, the trigger for the shift remains unclear and injects a greater-than-usual degree of instability to the path of UK monetary policy.

Politics remains a risk factor for the currency, both at a domestic level where speculation around PM May’s grip on the Tory party and a potential leadership challenge has increased and externally on the Brexit front where the risk of deadlocked UK/EU negotiations going into the December summit and a UK walkout has grown.

These risks are not mutually exclusive either, with a messy feedback loop from Brexit politics to BoE policy potentially exacerbating bearish currency pressures, widening the range of possible outcomes and imparting a fat left tail to the distribution. Yet current levels of GBP implied vols/skews price in almost no policy uncertainty premium.

A simplistic pointer is that GBP ATM vols and skews have retraced more than 100% of their post-Brexit referendum widening from last year even as the pound has reset at a permanently weaker level. A more robust argument is that current GBP vol levels are consistent with zero risk premium in the spot, where the latter is measured as the undershoot relative to a pure interest rate based cyclical framework.

As per the above charts, it demonstrates, the risk premium for policy uncertainty in the currency – both in cash and in vol –is near zero, and this is surprisingly equally, if not more, true for low-delta risk reversals that generally act as reliable repositories of tail risk premium. Thus, it is reckoned that the UK policy uncertainty inadequately priced into GBP options. Courtesy: JPM