Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

The Black–Scholes model has been accredited as a vivid breakthrough in asset pricing theory. But in applying it to real world options, problems immediately arose, because the volatility that makes an option’s model value consistent with its market price is different for different strike prices: thewell-knownn “volatility smile.” Over time, the smile evolved into a more monotonic, downward-sloping “skew,” and traders became comfortable with the idea of modeling its behavior and describing option market conditions in terms of the level and skew of implied volatilities.

A standard explanation for the skew is that the return distribution is not lognormal; in particular, it generally has a negative third moment (i.e., negative skewness). The similarity of the terms and the (potential) connection between the volatility skew and statistical skewness is one source of confusion. Another is that (unlike skewness) there is no standard measure for the volatility skew.

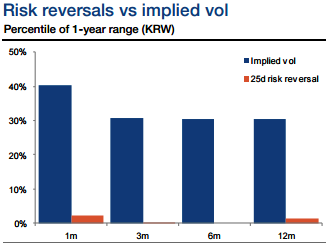

The skewness appears to be very depressed in KRW despite the elevated implied volatilities.

The KRW implied vol (1m to 1y) is in the middle of the 1-year range whereas 25-delta risk reversals are at the very bottom end.

The difference is even more marked in MXN, where implied volatility is at the top end of the 1-year range but risk reversals are close to the low point across the 3m-12m tenors.

As such, risk reversals could be a cheaper way to own volatility or position for tail risks compared to dollar calls.

However, for both MXN and KRW the beta of skew to moves in spot has fallen dramatically in recent years and in the case of MXN has plunged into negative territory.

It is explored that these issues and reviews a number of common skew measures. One significant result is that most of them vary strongly with the level of volatility, making comparisons across different underlying assets or over time difficult. After examining several performance measures, it is suggested that the most useful measure of the volatility skew is the difference between the implied volatilities for a 25 delta put and a 25 delta call, divided by the implied volatility for a 50 delta option.