Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

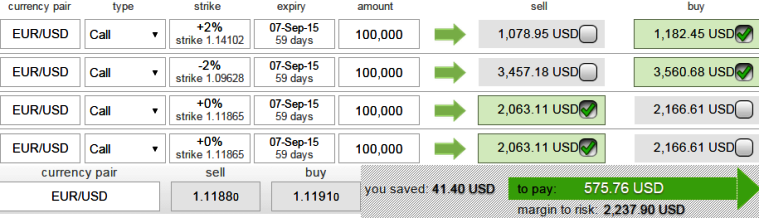

For those who don't like to accumulate either existing shorts on EUR positions or not longs dollar side with minimal delta terms, instead, better to take long term neutral positions such as option butterflies. We have some smart trading arrangements; these can even be utilized in our model the assortment of portfolio until the better clarity on how these global factors (especially Greece on euro side & Fed's decision on dollar side) will play out.

Therefore, buying 2M (+2%) Out-Of-The-Money (strikes at 1.1412) 0.34 delta call, buy another 2M (-2%) In-The-Money (strikes at 1.0964) 0.67 delta call and simultaneously sell 2 lots of 2M At-The-Money calls with positive theta values. All the positions should be early September maturities. As the delta on butterflies would usually be zero, this option combination should also be close to zero.

We reckon, this butterfly spread is best suitable and enables market laggards, risk averse traders, speculators who've been bias on both Fed's hike news and Grexit matters to participation in market turbulence as it brings in limited returns and limited risk.

Hedgers whose is neutral on irrespective market making matters but involved with their international business, this would arrests systematic risks.

Long butterfly spreads are entered when the investor thinks that the underlying exchange rate will not rise or fall much by expiration. One additional long position would result in net debit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Laggards who expect Fed’s hike in September hedge EUR/USD using long butterfly

Friday, July 10, 2015 12:33 PM UTC

Editor's Picks

- Market Data

Most Popular