World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch

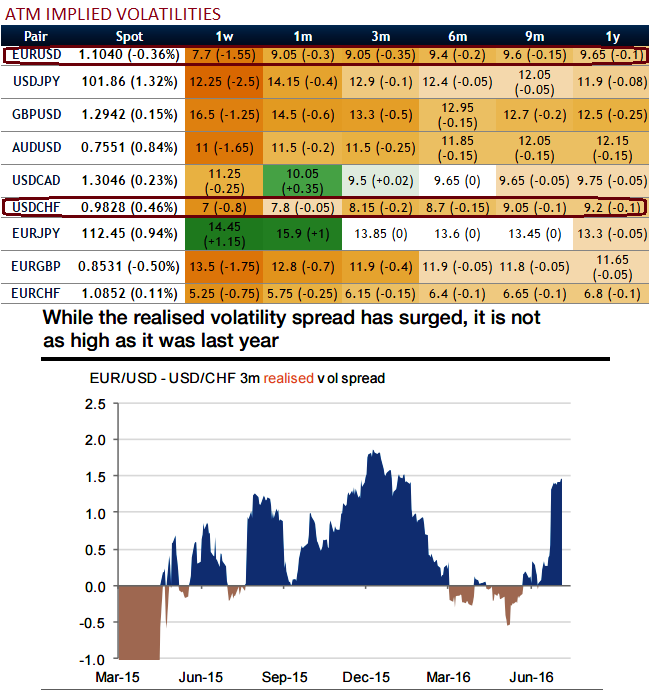

Further divergence between EUR/USD and USD/CHF volatility A spread of volatility swaps is exposed to the volatility differential between two currency pairs. Investors holding the position until the 3m expiry face unlimited losses if the realised volatility between EUR/USD and USD/CHF eventually exceeds 0.7 vols.

As we expect the vol spread to converge towards a flat level, it is advisable to go long in USD/CHF vs shorts in EUR/USD 3m volatility swaps, indicative bid: receive 0.7 vols.

However, past patterns suggest that the realised vol of the spread could exceed 0.7 vols (see above graph).

As such, we recommend unwinding the position before the expiry as soon as the net profit exceeds 0.5 vols.

Long/short of volatility swaps as a pure volatility trade, we recommend getting a pure volatility exposure via a long short of volatility swaps.

It allows for getting rid of systemic delta hedging and more generally of most of the gamma risks.

The pay-off of these instruments depends on realised volatility but their market to market (vega) is sensitive to implied volatility as well.