Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise

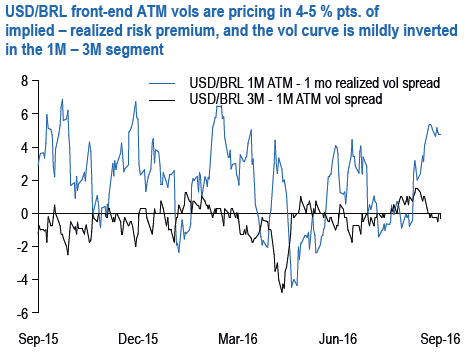

Rare currencies where we do not mind earning the fat vols carry on offer is BRL. Front-end USDBRL vols have popped higher over the past two weeks alongside a bounce in the spot, and are once again packing in sizeable 4-5 % pts. of premium in relation to trialing realized vols (see above chart).

At the same time, the BRL vol curve has mildly inverted in 1M – 3M expiries such that it has become economically viable to sell gamma hedged with vega longs via vega-neutral short 1M vs. long 3M straddle calendar spreads.

The fundamental case for vol selling in BRL rests on both the substantial risk premium on offer and a constructive take on currency macro.

We prefer more cautious calendar approach to short gamma than outright straddles since cash length in BRL is more extended than before after months of portfolio inflows creating risks of whipsaw risk on a technical short USD squeeze.

Directional investors not given to delta-hedging can consider buying calendar spreads of USD call/BRL put one-touch options instead of straddles.

For instance, short 1M vs. long 2M 3.40 strike USD call/BRL put one-touch calendars cost a net premium of 16% on mid (equal notionals/leg).

Assuming unchanged markets in a month’s time, the 1M 3.40 expires worthless and the 2M 3.40 rolls up to 40%, resulting in an acceptable static carry / payout ratio of 2.5 times.