2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

GBP’s performance in recent months was noticeable than analysts had anticipated on a blend of less immediate tail risk from Brexit (following outline political agreement in December over a stand-still transition once the UK leaves the EU next March until end-2020) and a more constructive central scenario for the economy and monetary policy. Of the two, a reduction in the Brexit risk premium appears to have been the more significant.

Nevertheless, the modest acceleration in UK growth to around 2% doubtless contributed to the reversal of speculative positioning in GBP from heavily short to heavily long (more so CTAs than macro investors we believe) as it led to a firming up of UK rate expectations (one and a halfhikes are now priced for the end of 2018, three and a half by end-2020) and the promotion of GBP to the vanguard of currencies where central banks are in the early stages of policy normalization.

Impressions though can be misleading, certainly as far as Brexit is concerned.

In our view, the medium-term prospects for Brexit and by extension GBP remain in a state of uncertain political flux. Investors may have assumed that a transition was a done deal but there are substantive aspects of the transition (the Irish border, migration) on which the UK and EU have not been able to agree (because they are so politically charged for a fragile Conservative government) and which prompted the EU’s chief negotiator to warn last week that a transition was not a given. A non-negotiated cliff-edge Brexit may be a very low probability event but that probability is not zero.

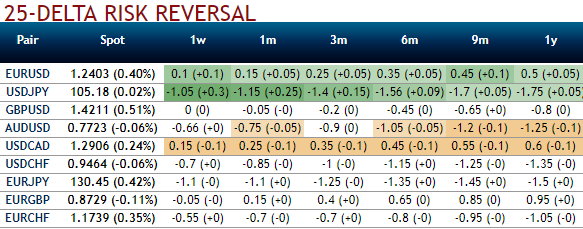

OTC indications (GBPUSD):

Let’s glance on sensitivity tool, there is no shift in risks reversals of GBP crosses in both shorter and longer tenors that indicates hedgers are factoring in above stated driving forces to their exposures, while the momentary bullish risks are seen in underlying spot FX prices, while long-term bearish hedging sentiments remain intact.

Positively skewed IVs of 2m tenors have been well balanced that signifies the hedging interests on both OTM put/call strikes that means the ATM instruments have a higher likelihood of expiring in-the-money, while balanced hedging sentiments on either side in comparatively shorter tenors are favorable to both call and put options holders’ advantages.

Whereas the 6m skews have still been indicating bearish risks, this stance is substantiated by the bearish neutral risk reversals that indicate hedgers still bid for downside risks. ATM IVs are still stuck between 8.10-8.30% ranges for 3-6m tenors.

Currency Strength Index: FxWirePro's hourly GBP spot index has turned to -98 (which is bearish), while hourly USD spot index was creeping up at shy above -62 (bearish) while articulating (at 08:29 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: