Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

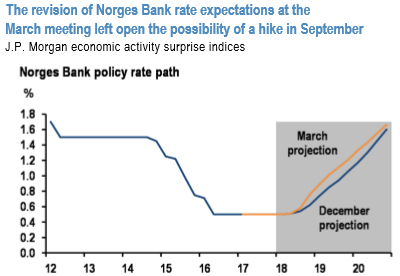

Norwegian krona bulls have received a fillip over the past two weeks from a hawkish re-assessment of the central bank’s rate track and a sharp rally in oil prices. The Norges Bank signaled at its March meeting that policy rates would rise earlier than 1Q’19 as had been previously assumed (refer 1st chart), which in our economist’s view is consistent with a first hike in September.

The central bank has revised up its policy rate profile by 15bp and 6bp for the end of 2019 and 2020, even though it has taken down its CPI forecast by 0.16%pts and 0.33%pts for those horizons, indicating a real policy rate that is effectively 31bp and 48 bp higher for the end 2019 and 2020, respectively. This puts the Norges Bank in sharp contrast with most other G10 central banks that have adopted a more dovish tone.

In addition, Brent also rallied $5/bbl this week in part on supportive inventory data and partly on geopolitical concerns relating to US' commitment to the Iran nuclear deal. Please be noted that odds of production curbs continuing beyond June have increased with OPEC considering a technical change of using 7-yr average inventory levels instead of the current 5-yr to benchmark progress on supply re-balancing, which would result in current stocks looking appreciably above target and in need of further reduction.

We took part profit on our long NOKSEK position in cash after last week’s Norges Bank fueled rally, but remain in short EURNOK cash and a NOKSEK vs EURSEK option switch to milk the residual cheapness in the cross that screens a couple of points cheap relative to contemporaneous interest rate and energy price drivers even after this year’s run-up (refer 2nd chart). Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: