‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  China Trade Surplus Beats Forecasts in July as Exports Stay Strong

China Trade Surplus Beats Forecasts in July as Exports Stay Strong  Iran-Oman Near Strait of Hormuz Deal as Shipping Tensions Persist

Iran-Oman Near Strait of Hormuz Deal as Shipping Tensions Persist  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears

Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Oil Prices Rise as Hormuz Reopening Remains Uncertain

Oil Prices Rise as Hormuz Reopening Remains Uncertain  Japan Posts First Current Account Deficit in 17 Months as Dividend Payments Surge

Japan Posts First Current Account Deficit in 17 Months as Dividend Payments Surge  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

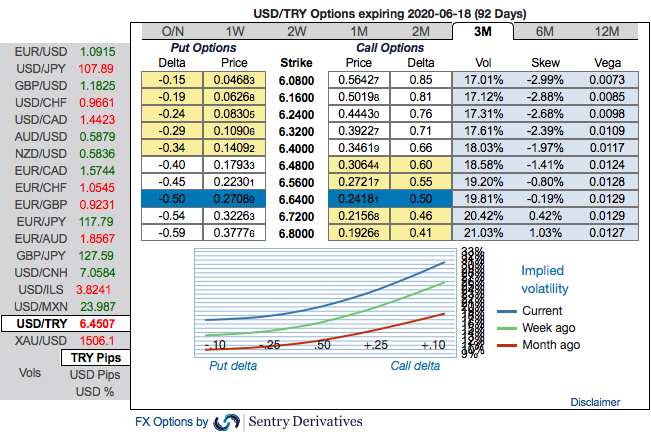

Turkey's central bank pulled forward a scheduled MPC meeting by two days and implemented a 100bps emergency rate cut yesterday. The CB reduced the 1-week repo rate from 10.75% to 9.75% and lowered RRR on all FX deposits by 500bps (for banks which are meeting loan growth criteria); CBT will also provide liquidity to banks using special intraday and overnight facilities as well as 91-day repos if necessary. CBT has increased the liquidity limit on primary dealers, which means that it will effectively fund them at 8.25% instead of the 9.75% policy rate. Having witnessed similar packages launched in recent days by major world central banks as well as several emerging market central banks, NBP for example, CBT's measures fall within a 'reasonable spectrum'. Such measures are being used to mitigate the worst side-effects of the coronavirus outbreak; they are, of course, not intended to solve the underlying healthcare problem, just dampen the collateral damage to the economy. Turkish GDP growth and inflation will both fall in coming months; at this time, the usual consideration of above-target inflation warranting higher interest rates is temporarily on hold. Rate cuts are more likely to have a positive impact on the currency because, without monetary easing, the economy would contract even more. This is why the lira outperformed peers notably following the announcement.

Since the latest data tell us that longstanding Turkish risks still persist, and meanwhile the real interest rate is going to negative, we should look for a sharp rise in USDTRY in coming months.

Hedging Strategy:

On hedging grounds, capitalizing on prevailing price dips and above driving forces, we already advocated 2m USDTRY debit call spreads with a view to arresting momentary downside risks and upside risks in the major trend. At spot reference: 6.4511 level, initiated 2m 6.05/6.80 call spreads at net debit. One can achieve hedging objective as the deep in the money call option with a very strong delta will move in tandem with the underlying spikes.

It seems that hedgers of TRY are positioned for the upside risks on the above fundamental factors. The skewness in 3m IVs are still indicating upside risks, higher bids for OTM calls are hedging bias towards upside risks (refer above nutshell).

IVs of this underlying pair is also on the higher side, trending highest among the G20 FX space. Call options with a higher IVs cost more, because, increasing IV is conducive for the option holder, just for an intuition that the higher likelihood of the market ‘swinging’ in holder’s favour. Courtesy: Sentry & Commerzbank