Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

The fears of a recession with weakening yields, massive losses on the stock markets, concerns about a government shutdown that could be on the cards today if the Senate is awkward, and another minister throwing in the towel and leaving the Trump administration – all events that are eroding confidence in the dollar at present. Therefore, it is likely to start into the Christmas period on the back foot.

While the drop of USDJPY 1Y vol below 8.0 even as macro markets were buffeted by a near-recessionary trifecta of yield curve flattening, credit spreads widening and sell- off in equities over the past two months has not escaped investors’ attention. 8.0 is not a line in the sand for 1Y yen vol by any stretch; we are through this year’s January lows, and the mid-2014 trough of 7.0 looms as the next major target, beyond which there is still substantial room to fall to re-test pre-GFC levels in the 6s. It is difficult to argue with option prices steadily softening when spot is stuck in a tight 112-114 range and delivering 2-2.5 pts. below implieds.

There is also a case to be made that the ongoing softness in yen realized vols can continue longer than some anticipate, since the propensity of the yen to rally in market downturns is being dampened by cyclically wide US – Japan interest rate differentials that we reckon are fuelling above-average investment outflows and reduction in FX hedge ratios of traditionally well-hedged foreign bond purchases. Anecdotal evidence suggests that such realized vol drags are being exacerbated by drip supply of vega from Japanese importers who are reloading / adding to USD-buying FX hedges with embedded short optionality on downticks in USDJPY spot.

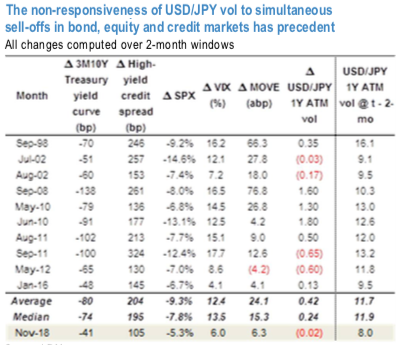

Finally, the insensitivity of yen vols to recent macro developments is not without historical precedent.

The above chart shortlists a handful of months that experienced risk-off moves in yield curves, credit spreads and SPX over the past 25 years equal to or greater than that of the past two months, and shows that 4 out of the 10 episodes before this year saw yen vol fall rather than rise in response to macro risk-off triggers, though admittedly all from initial levels well north of the current 8%. Courtesy: JPM

Currency Strength Index:FxWirePro's hourly JPY spot index is flashing at 83 levels (which is bullish), hourly USD spot index was at -5 (neutral) while articulating at (13:30 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex