US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

The decline of FX vol levels after the late July spike has continued steadily over the past few weeks, under the powerful influence of dovish major Central Banks quenching global recession fears, and as the market has started to price in an imminent US/China trade deal.

In this context, FX short-Gamma strategies have delivered solid performances, with the benchmark portfolio we monitor of 1M 25-delta strangle strategies up 9.7% so far in 2019.

Our tactical filtering model, which has helped cutting the August drawdown at the expense of a slightly lower yearly performance (+8.0%), remains heavily biased towards short-Gamma, with the latest average signal at 89% of the max short-Gamma trade allowed.

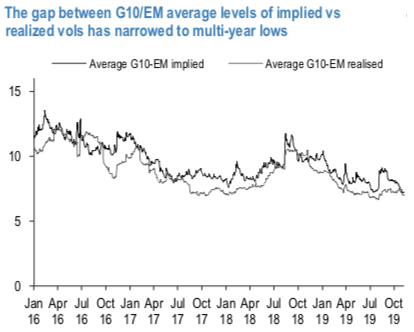

A natural benchmark for judging on the valuation of implied vol levels regards the level of realized volatilities; when averaging over liquid G10/EM USD pairs (refer 1st chart), the gap between the two, or vol premium, has narrowed to multi-year lows. Also, while the August spike of implied vols proved to be short-lived, realized vols exhibited some resilience over the period, leaving less room for dropping lower, unless new market micro-structure forces were to come into play. From this perspective, room for further declines of vol levels, and consequently for further short- dated gains of short-Gamma strategies, appears to be limited at the moment.

We have recently introduced a macro model linking FX vol levels to the underlying rates vols/correlation dynamics. The model (refer 2nd chart) has done a pretty decent job in terms of tracking the evolution of vol levels over time. The average vol level is undervalued by 3 standard deviations based on the model, but in vol terms (7.3 vs 8.2), this amounts to less than 1 vol point. So, from this standpoint, while we see room for a marginal repricing higher of vol levels, potential is fairly limited.

The two analyses above point to a relative balance between opposite forces driving FX vols: absent major surprises on the trade front, one could expect some near-term stability as far as FX vol levels are concerned. In the following, we’ll investigate how the current interplay of pricing parameters in a low vol market can guide in the search of directional option plays. Courtesy: JPM