AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

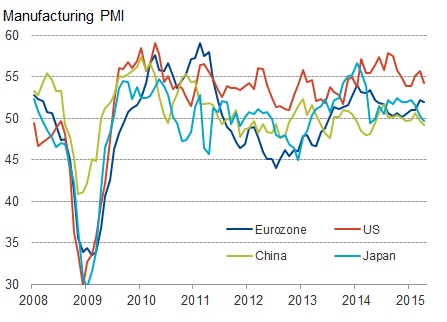

Yesterday's provisionary April PMI report might have cheered the bears calling for an end to recovery, however it would be premature to call for such, in spite recent weakness.

PMI above 50 indicates growth.

- Japanese PMI dropped to 49.7 from 50.3 prior.

- Chinese PMI dropped further in negative growth zone to 49.2 from 49.6 prior.

- Euro zone manufacturing PMI dropped to 51.9 from 52.2

- US manufacturing PMI dropped to 54.2 from 55.7 prior.

However, don't read too much into the weak PMI, growth historically has been uneven similar to market's rise and fall. World as of now, is far past the crisis slump and economic activities will keep improving over the coming time.

- New export orders continue to rise for tenth consecutive month in Japan. Employment also improved.

- Export orders reversed course in China, ending its three months of consecutive drop.

- April registered strongest monthly gains in employment across Eurozone, manufacturing slowed but business at service sector continue to improve at solid pace.

- Despite headwinds from dollar, production volume still moving up and employment remains solid across sectors in US.