Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  China Trade Surplus Beats Forecasts in July as Exports Stay Strong

China Trade Surplus Beats Forecasts in July as Exports Stay Strong  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  Asian Currencies Steady as Markets Await U.S. Jobs Data

Asian Currencies Steady as Markets Await U.S. Jobs Data  Trump Unveils $3 Billion U.S. Critical Minerals Push

Trump Unveils $3 Billion U.S. Critical Minerals Push  Dollar Holds Near Six-Week Low as Yen Loses Momentum Ahead of U.S. Jobs Data

Dollar Holds Near Six-Week Low as Yen Loses Momentum Ahead of U.S. Jobs Data  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

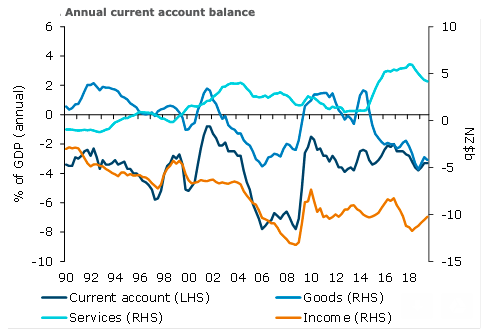

New Zealand’s annual current account deficit widened slightly from $10.2 billion in Q2 to $10.3 billion in Q3. In ratio terms, it was unchanged at 3.3 percent of GDP.

In seasonally adjusted terms, the current account deficit widened $0.3 billion from Q2, led by a widening goods deficit, as exports fell and imports lifted. New Zealand’s net international liability position widened $6 billion from Q2 to $172.8 billion, and widened 1.4 percentage points as a share of GDP to 56.3 percent.

The goods balance posted a deficit of 1.4 percent of GDP, versus a long-run average of +0.7 percent, reflecting still-buoyed demand for imports on the back of robust domestic consumption. The services balance posted a surplus of 1.3 percent of GDP, above its historical average of +0.8 percent, supported by solid growth in tourism exports over the past few years (despite some recent slowing).

And the income deficit of just 3.3 percent of GDP remains narrower than its historical average of 5.1 percent, reflecting low interest rates globally.

The unadjusted goods balance fell from surplus into deficit (from $0.9 billion to -$3.5 billion), as expected, with exports falling and imports lifting. Log and dairy led the decline in goods exports, more than offsetting a lift in the goods terms of trade (if the OTI is anything to go by). Meat prices in particular are benefiting from significant supply disruptions in China’s pork industry.

"The goods deficit is expected to remain broadly stable as a share of GDP. The lower NZD should dampen growth in import volumes, but softer global growth should keep world import prices subdued, providing an offset. Still-elevated net migration and a buoyant household sector will suck in the imports. On the exports side, constrained global dairy supply and demand for pork alternatives in China should keep meat and dairy prices elevated (more than offsetting slightly weaker NZ dairy production this season). But downside risks from weaker global demand remain," ANZ Research commented in its latest report.