How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

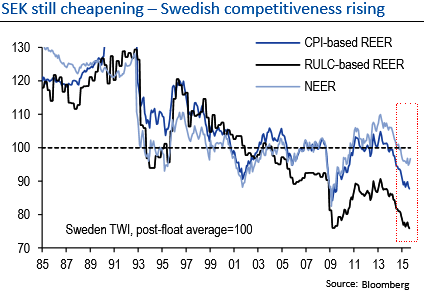

SEK has transacted sturdily through November and early December months, gaining against almost all G10 currencies. But took a U turn again in New Year series, further gains from here onwards would be more challenging, however, with EUR/SEK back in the 9.35-9.45 zones that the Riksbank has previously shown great discomfort with (not least with March's intra-meeting rate cut).

Despite SEK strength, the central bank stood pat to leave rates unchanged at the December 15 meeting and also left its forward guidance unchanged, the profile implying a material risk of another cut in early-2016.

Governor Ingves also stressed that -0.35% should not be seen as a floor for policy rates. Looking forward, we think the Riksbank will remain sensitive to exchange rate movements in early-2016. In large part this reflects the importance of the spring wage round, when around two thirds of the labour force will settle wage deals, many of them lasting for three years.

Low headline inflation readings through the negotiations would run the risk of employees locking into low wage growth for a prolonged period, making it more difficult for the Riksbank to hit its medium-term inflation target of 2%. For this reason, and given the Riksbank's apparent preference for keeping EUR/SEK above 9.20, our bias is for a softer SEK into Q1.

Owing to crude prices, NOK continues to trade ailing prices lower, with EUR/NOK retesting the year's high above 9.74 and NOK/SEK fell to a 23-year low. The significant easing of policy through the exchange rate was probably a key reason for Norges Bank leaving rates on hold at its December 17 announcement, despite a further 15% fall in crude prices since the previous meeting.

Going forward, Norges Bank's guidance is signaling another rate cut, and with rates still 0.75% above the zero bound, it clearly has more scope to deliver than other central banks in Europe. Domestic data are certainly no impediment, with onshore GDP barely positive in Q2 and Q3, and the high level of core inflation (3.1% y/y) largely due to import prices. While this risk remains and until we are confident crude prices have formed a base, we continue to see the risks to the upside for EUR/NOK.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Scandis FX space still looks vulnerable in H1 2016

Thursday, January 28, 2016 12:00 PM UTC

Editor's Picks

- Market Data

Most Popular