Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

US unemployment rate stands at 5.5%, hovering close to level considered normal by Economists and US Federal Reserve. Average of initial jobless claims have reached multi decade low.

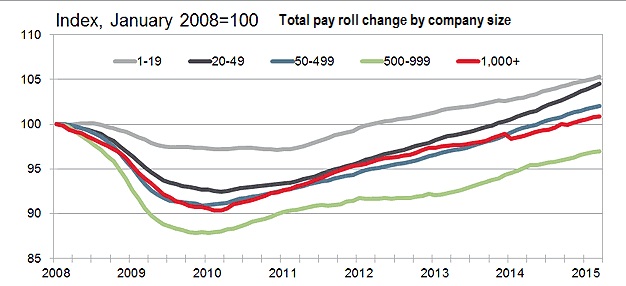

- Still not all the employment indicators have reached close to normal or even pre- crisis level of 2008. Payroll gains and unemployment rate varies widely among industries and size of companies.

As shown in the chart, payroll gains at large companies with employee base larger than 1000, contributed not only less to pay roll gains, is yet to reach pre crisis level. Most of the gains are driven by companies with fewer than 50 employees.

This divergence is partially due to lacklustre demand globally as large companies tend to operate on economies of scale.

- Moreover jobs added by professional and business services remain solid, jobs in construction and manufacturing remains weaker then pre-crisis level.

Manufacturing lag is partially due to automation, whereas housing and mortgage sector remain somewhat weaker than prior.

US Federal Reserve would very likely deliver at least one rate hike this year, however pace of hike would be very gradual as FED would wait for recovery and job gains to speed up in the following sector.

So even with a rate hike delivered dollar's rise would not be one way ride. Dollar index is trading at 94.85, down -0.30% today so far.