Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Gold Prices Rise as Fed Rate Hike Bets Ease

Gold Prices Rise as Fed Rate Hike Bets Ease  Gold Prices Hold Near Seven-Week High as Markets Await U.S. Inflation Data

Gold Prices Hold Near Seven-Week High as Markets Await U.S. Inflation Data  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  UK Retail Sales Rise as World Cup and Heatwave Boost Food, Pubs and Clothing

UK Retail Sales Rise as World Cup and Heatwave Boost Food, Pubs and Clothing  Singapore Raises 2026 GDP Growth Forecast as AI Demand Fuels Economy

Singapore Raises 2026 GDP Growth Forecast as AI Demand Fuels Economy  European Stocks Flat as Oil Prices Rise, US CPI in Focus

European Stocks Flat as Oil Prices Rise, US CPI in Focus  Gold’s Bull Run Intact: Safe-Haven Bids Overpower Treasury Yield Pressure

Gold’s Bull Run Intact: Safe-Haven Bids Overpower Treasury Yield Pressure  China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases

China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases  Goldman Sachs Sees US Stock Buybacks Outpacing Equity Issuance as AI Funding Rises

Goldman Sachs Sees US Stock Buybacks Outpacing Equity Issuance as AI Funding Rises  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

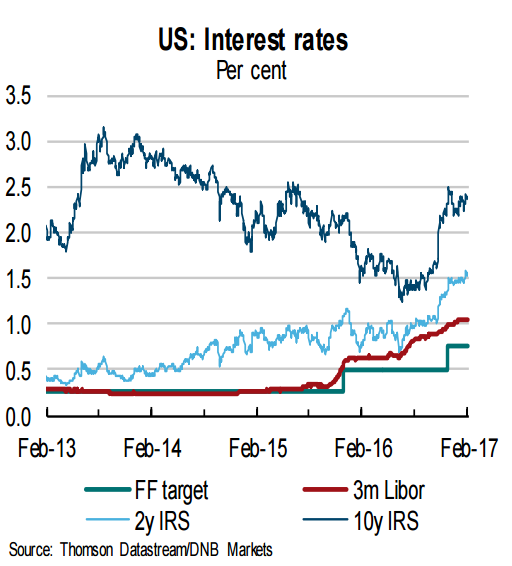

Minutes of the Federal Reserve's Jan. 31-Feb monetary policy meeting published earlier this week on Wednesday showed that many policymakers believed another interest rate hike might be appropriate "fairly soon" if labor market and inflation data meet or beat expectations. Most members expect a continuation of moderate expansion in economic activity and a gradual rise in inflation to target over the medium-term.

Data released on Thursday showed that U.S. initial jobless claims for the week ending February 18 rose slightly last week by 6,000 to a seasonally adjusted 244,000. It was the 103rd straight week that claims remained below 300,000, a threshold associated with a healthy labor market. The four-week moving average in initial claims, considered a better gauge, fell modestly, to 241,000 from 245,000, in a sign of a strengthening labor market.

"Altogether, we see little in the recent jobless claims data to change our view on labor markets. Despite some volatility in the data around year-end, the claims data continue to point to a low rate of separation activity in labor markets and are suggestive of favorable labor market conditions overall." said Barclays capital in a report.

The next payrolls report will clearly be key, but we also have a stream of speeches from Fed speakers between now and the 16 March decision which will be important for shaping expectations. Furthermore, the core PCE inflation release for January, due 1. March will also be important. Fading optimism surrounding US President Donald Trump's proposed fiscal policies dimmed prospects of a Fed rate hike move at its upcoming meeting in March.

"We maintain our call for two hikes in 2017 - most likely in June and December," said Knut A. Magnussen, Senior Economist DNB Markets.

Markets were looking for a firmer signal from FOMC minutes and were left disappointed after the release. The USD sold off and bonds rallied post the release on Wednesday. Thursday's comments from Treasury Secretary Steven Mnuchin, providing little details for the proposed tax reforms, did little to ease market concerns. Broad-based US Dollar selling extends on third consecutive session. USD/JPY was trading at 112.33, while EUR/USD was at 1.0607 at 1200 GMT.

FxWirePro's USD hourly strength index was bearish at -70.1237. For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.