Oil Prices Slip as Hormuz Shipping Progress and Rising U.S. Crude Stocks Weigh on Market

Oil Prices Slip as Hormuz Shipping Progress and Rising U.S. Crude Stocks Weigh on Market  Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan

Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  Australia Trade Surplus Returns in June as Iron Ore, Coal and LNG Exports Surge

Australia Trade Surplus Returns in June as Iron Ore, Coal and LNG Exports Surge  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  US Stock Futures Hold Steady as Iran Hormuz Deal and Earnings Shape Market Sentiment

US Stock Futures Hold Steady as Iran Hormuz Deal and Earnings Shape Market Sentiment  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns

Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow

Gold Price Hits Seven-Week High as Fed Rate Hike Bets Fade and Hormuz Deal Hopes Grow  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Philippine GDP Growth Slows to 2.3% in Q2

Philippine GDP Growth Slows to 2.3% in Q2  US Stock Futures Rise as Markets Await July Payrolls Data

US Stock Futures Rise as Markets Await July Payrolls Data  Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff

Singapore Says One-Third of U.S. Exports Hit by New 12.5% Tariff  Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

The point is, ladies and gentleman, that greed – for lack of a better word – is good. Greed is right. Greed works. Greed clarifies, cuts through, and captures the essence of the evolutionary spirit. Greed, in all of its forms – greed for life, for money, for love, knowledge – has marked the upward surge of mankind.

– Gordon Gekko, Wall Street 1987

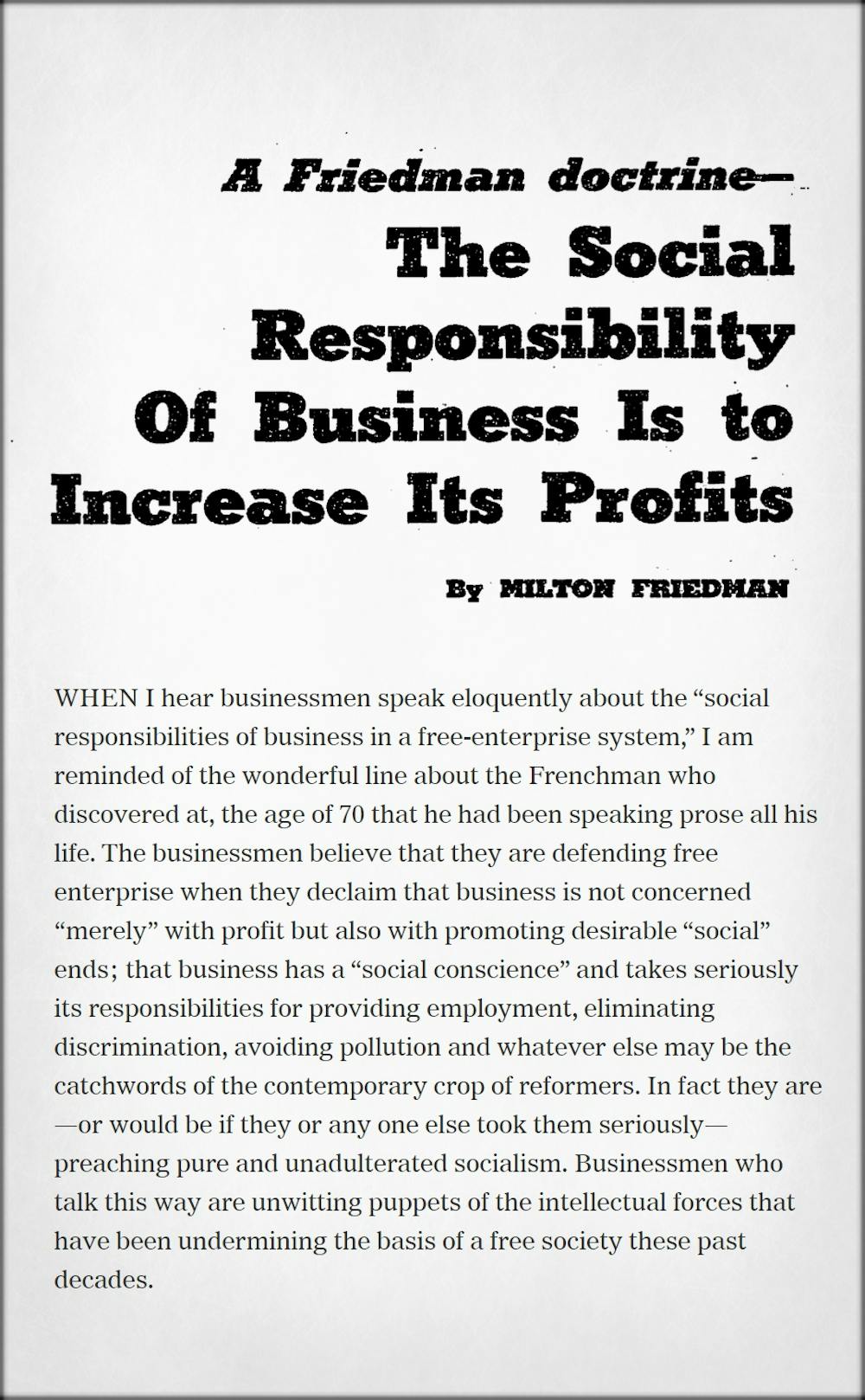

Fifty years ago, well before the movie Wall Street, Chicago economist Milton Friedman set down what for many was the essence of the famous speech in Wall Street in an article for the New York times magazine entitled “The Social Responsibility of Business is to Increase its Profits”.

His point, which along with his other contributions was recognised when he was awarded the Nobel Memorial Prize in Economic Sciences in 1976, was that businesses serve society best when they abandon talk of “social responsibilities” and solely maximise returns for shareholders.

Incredibly influential (the past week has seen special conferences and anniversary analyses), the essay has been credited with ushering in the doctrine of “shareholder primacy,” and with it short-termism, hostile takeovers, colossal frauds and savage job cuts.

Its a doctrine not seriously challenged until the 2008-2009 global financial crisis.

The essay that sparked a revolution, 50 years ago this week. New York Times

But in an important respect it was misread.

Although not clear from the title of the essay, Friedman himself was quite concerned with broader social aims.

His essay was about how best to achieve them.

His point was that if companies made as much money as they could for their shareholders, those shareholders could spend it on social goals, “if they wished to do so”.

For the company to attempt to guess what goals its shareholders would want to support and to support them itself would be for the company to do its main job badly.

Although it made a certain sort of sense, the Friedman doctrine has turned out to be incomplete.

As Harvard University’s Oliver Hart (who also won the Nobel Prize for Economics) has points out, corporations are often much better than their shareholders at achieving the goals their shareholders care about.

Corporations can achieve more than individuals

Individual shareholders can’t do much to avert climate change, but the corporations they own can.

A mining company could either stop operating an environmentally-damaging mine or run the mine, make a bunch of money and pay it to shareholders who could use the money to mitigate the damage “if they wished to do so”.

Its hard to argue that, if shareholders do indeed “wish to do so”, the first option isn’t better.

To cite a recent instance, is hard to “un-blow-up” 46,000 years of Indigenous heritage.

In contrast, Friedman was almost surely right about corporate charitable contributions, which was in many ways the impetus for the article.

In what way are corporations better at giving money to charities (and political parties) than individuals. In none that are obvious (and not potentially corrupt).

So where do we draw the line about what corporations do and don’t do?

Proponents of the “stakeholder view” now endorsed by an increasing number of superannuation funds think corporations should have a composite objective that takes into account the interests of shareholders, bondholders, workers, suppliers, the environment, and more.

Yet a point in every direction…

The problem with this, as recognised by the arrow-covered pointless man in the animated Harry Nilsson film What’s The Point? is that “a point in every direction is the same as no point at all”.

As Friedman put it, composite objectives suffer from “looseness and lack of rigour”.

Others, such as Hart and University of Chicago professor Luigi Zingales think firms should find out what shareholders most want, and “pursue that goal.”

This has the virtue of permitting a social objective while creating a concrete, measurable goal.

It’s a way of giving shareholders (and super fund members) a voice that is more direct than simply electing directors every few years.

Friedman helped start an important discussion. Fifty years on, it isn’t finished.