Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

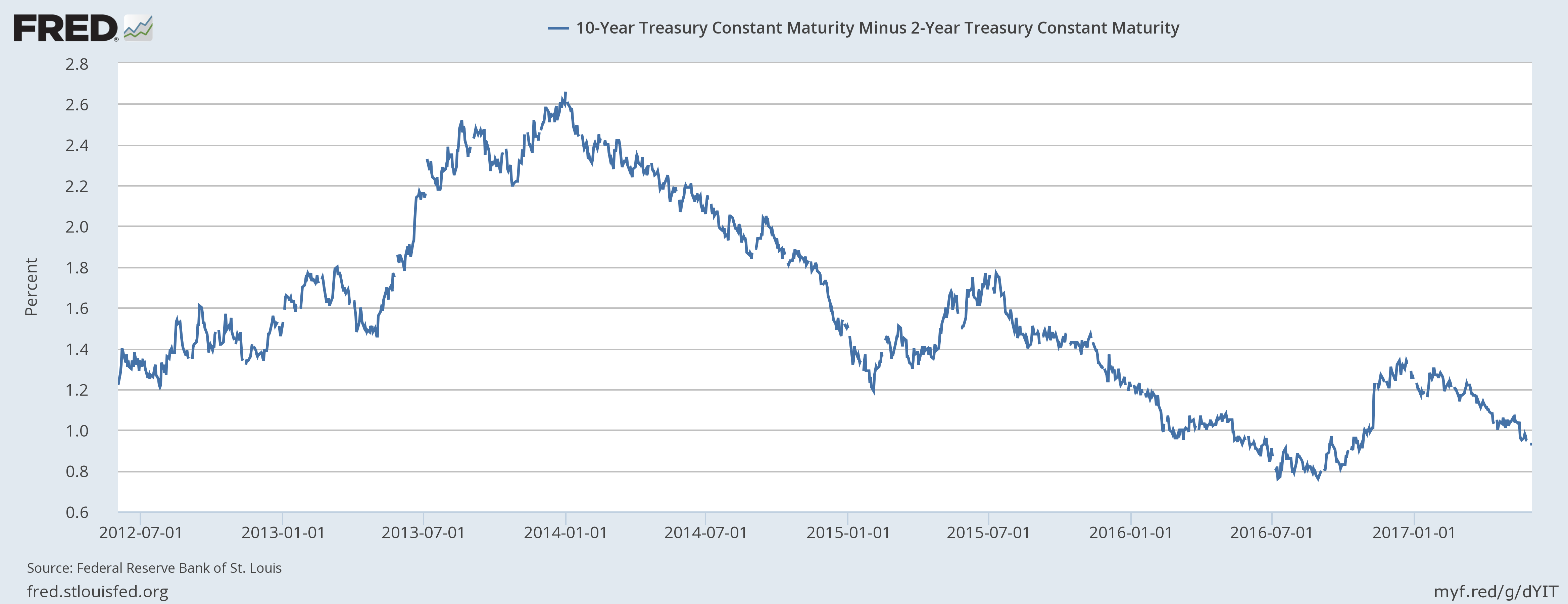

After President Donald Trump’s victory last November, the U.S. yield curve steepened sharply in anticipation of faster rate hikes by the U.S. Federal Reserve as traders anticipated higher inflation in the United States thanks to President Trump’s promise of increased infrastructure spending along with tax reforms and tax cuts. The gap between the U.S. 2-year Treasury yield and the 10-year Treasury yield jumped from just 100 basis points on November 8th to 133 basis points by December last year.

However, as Donald Trump Presidency remained dogged by controversies with related to Russia’s interference in the US election and high profile leaks aimed to undermine the current administration, traders have started pricing a slower path for President Trump’s promises through Congress. Moreover, the Democrats remain committed to undermining and voting down all of President’s agendas including the selection of his cabinet members. They are working to delay the selection of cabinet members as much as possible.

The recent weakness in the economic numbers has also contributed to the decline. Last Friday, non-farm payroll report showed that the U.S. economy added just about 138,000 jobs in the month of May, much lower than anticipated by the market and economists. The yield gap between the 10-year Treasury and the 2-year Treasury, which is often seen as a measure of duration risk linked to inflation and hike expectations has now declined to just 93 basis points, as of June 2nd, which is the weakest point since last October, marking an end of the ‘Trumpflation’ trade.