European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different

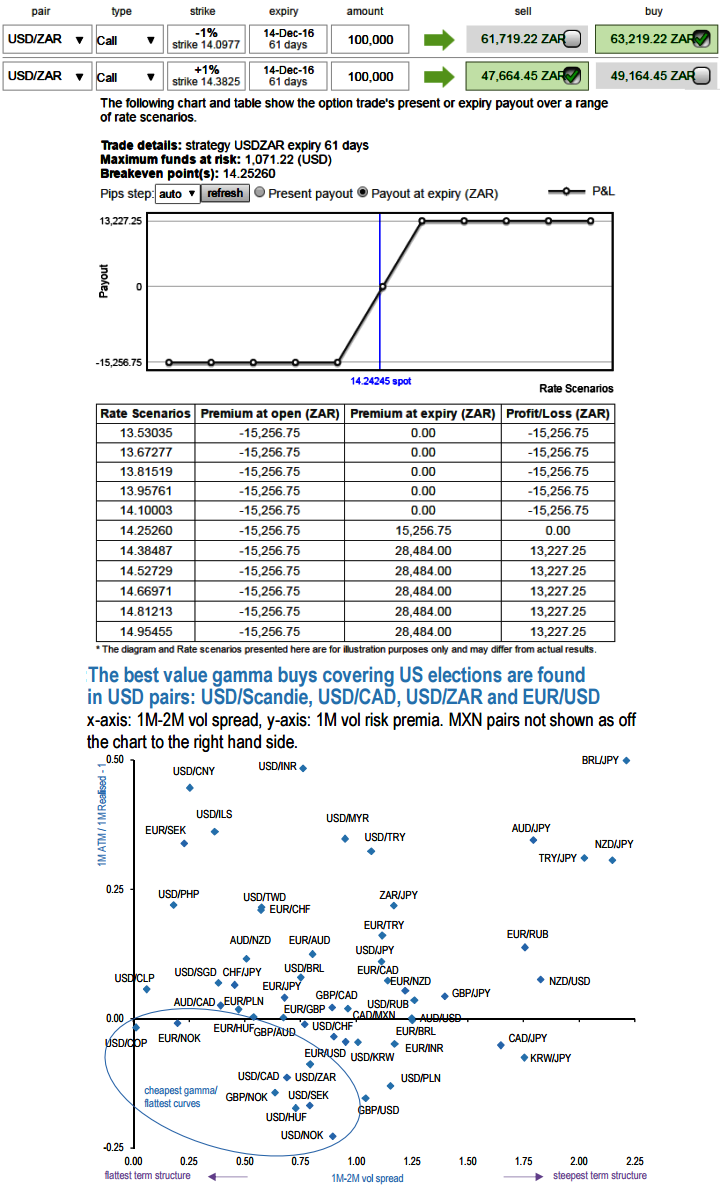

Nov/Dec US Elections and Fed calendars dominate the vol landscape until year end, dwarfing NFPs as vol risk events.

On the option trade front among EMFX, we recommend positioning longs in USDZAR as the South African significantly overshooting fundamentals –

Long USDZAR portfolios that make buying USD vols all the more appealing. Instead of naked vanilla call form we suggest call spread structure for the 2M horizon, optimizing strikes for leverage.

In USDZAR, the 1M-2M ATM spread is below average at +0.75, as 1M vols had remained relatively anchored and never softened significantly.

Therefore the premium for owning US elections risk isn't punitive, and the short leg further mitigates the cost of gamma (see above chart).

The above table explains how does the call spread is ordered in decreasing values of max payout/cost regardless of upswings.

We find that skews aren’t steep enough vs ATM to allow for a wide range of strikes to be efficient. In order to ensure more than 50% discount to the outright vanilla, and a max payout/cost higher than 3.5:1, one needs to choose a combination of long 40D vs 25D.

The call spread achieves a 55% discount to outright call and a max payout/cost ratio of 3.7:1 (mid values).

Please be noted that the tenors and strikes shown in the diagram are only for demonstration purpose, use appropriate tenors as suitable for your exposure.