Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Ahead of RBNZ’s monetary policy meeting that is scheduled next week, the market pricing for a November OCR cut has been stable during the past two weeks at around 80% (currently 86%).

Q3 CPI data was unsurprising to RBNZ forecasts, although it did surprise a number of analysts who expected something lower.

The markets have consistently priced in a greater than 50% chance of a November cut since Assistant Governor McDermott’s speech in September reminding all that the “promised” cut remains in the pipeline.

So what could spook them from cutting? A sharp rise in inflation expectations on 2 Nov (unlikely, given CPI is running at only 0.2%/yr), or a plunge in the NZD, come to mind. We continue to expect a cut on 10 Nov, followed by a lengthy pause.

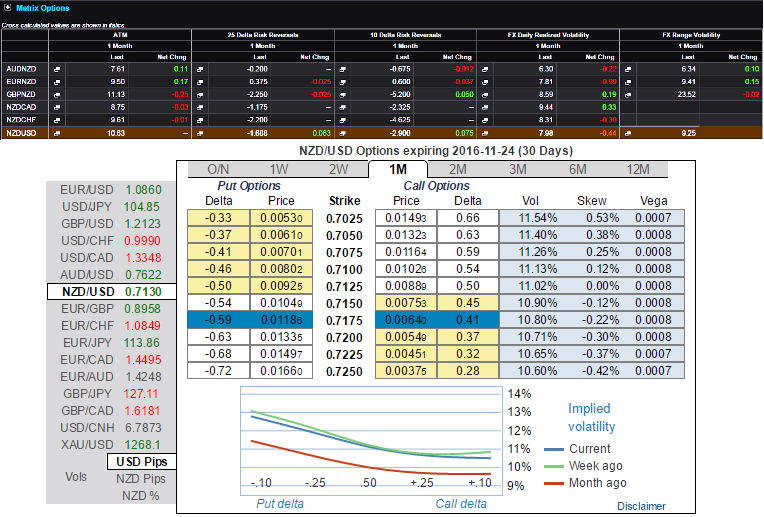

Consequently, the participants in NZD OTC market are getting active, 1m IVs are screaming off over 11.02% and positive skew is observed in OTM put strikes.

Implied volatility is elevated compared to realized volatility (see above nutshell), suggesting a structure selling it.

The downside skew is not sufficiently elevated to finance a put via low strikes (a put spread-like structure), but the negative skew is enough to obtain an attractive discount via a downside knock-out. Such a barrier is appropriate for trading moderate NZD/USD downside.