US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

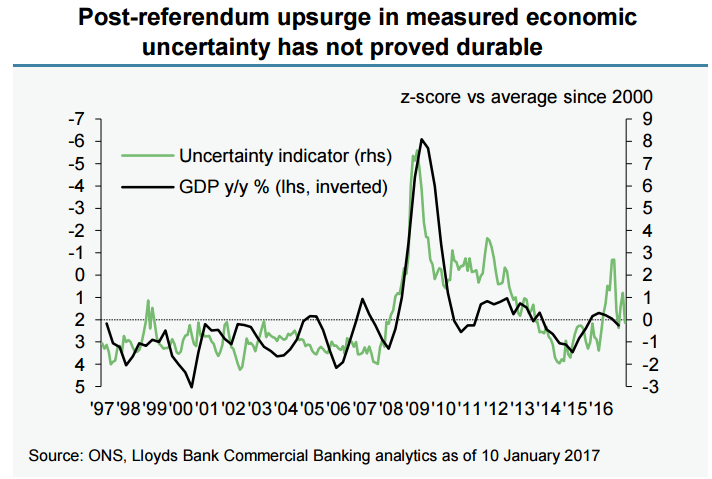

Incoming economic data in UK do not support the view of an uncertainty driven slowdown in the aftermath of the EU referendum. UK economy expanded at 0.6 percent q/q in Q3 2016, the first full post-referendum quarter. The economy’s dominant services sector saw a brisk 1.0 percent q/q growth in Q3.

Composite PMI in December spanning across the manufacturing, construction and services sectors stood at its strongest since July 2015. Survey data for Q4 have also been solid and analysts expect overall GDP growth in Q4 could post a 0.5 percent q/q rise. Together with the recent history of GDP data, that would leave growth in the six months since the referendum, in fact, quicker than in the first half of 2016. And the apparent resilience towards the end of 2016 suggests that some of this momentum is likely to carry over into H1 2017.

Inflation in the UK is likely to rise through 2 percent target by spring 2017 as currency weakness drives import price rises. The coming few months are likely to see a sharp rise in the headline inflation rate on the back of significant impact from energy price base effects and as the exchange rate pass-through becomes dominant.

"We expect CPI inflation to tick up further to 1.3% by December and burst through the 2% target by spring 2017. Easing underlying cost pressures from the second half of 2017 should provide some offset as growth in the economy slows modestly and reduced labour market tightness limits inflation’s overshoot relative to target." said Lloyds bank in a report.

As exit negotiations with the European Union begin, how measures of uncertainty evolve over the coming months and how strong the mapping proves with official activity data are among the key questions for the near-term outlook. The deceleration of economic activity over the course of 2017 and 2018 is likely to principally result from the weakness of sterling.

UK Monetary Policy Committee (MPC) is likely to look through inflation rise, but could react if activity slowdown proves more modest than expected. "Our base scenario sees Bank Rate on hold for the foreseeable future, but with a skew towards tighter policy," adds Lloyd's Bank in a report.

GBP/USD tests 1.21, weakest since Oct 7 'flash crash'. Cable continued slump as Hard-Brexit concerns continued to weigh on the investors’ sentiment. EUR/GBP spiked beyond 0.8750 to hit fresh multi-week highs at 0.8763.

FxWirePro Currency Strength Index showed Hourly GBP Spot Index at -91.9716 (Highly Bearish) at 1130 GMT. For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.