SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

On the verge of economic data announcements in Euro zone as shown below, volatility in currency tend to go up given the tension in the market and readjusting of portfolios.

Important data releases for today: German retail sales, French Consumer spending, Spanish CPI, and Italian Q1 GDP.

The change in volatility before and after announcements expresses the change of mood in the market. Hence, we have to observe and use Vega in our strategy as it measures the sensitivity of an option's value to a change in volatility.

After the data release, it often drops and even more so if the data was as expected.

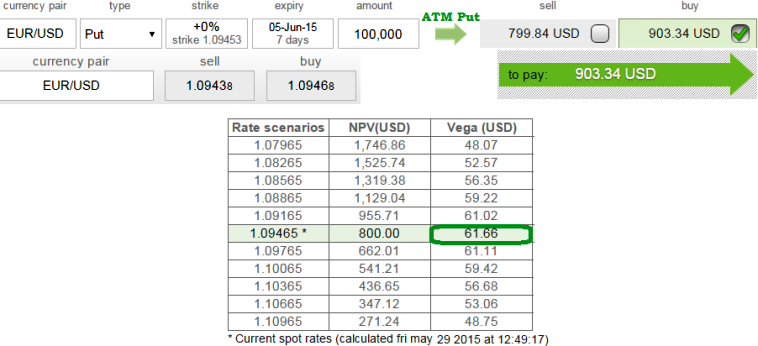

So if you expect EUR/USD to dip or remain range bound then you could look ahead to trade a long ATM with less Vega value naked put.

Here the put holder who has no desire to own the underlying currency as he expects it to slump in coming days.

The investor buys ATM put option with an anticipation that the price of the underlying currency will go significantly below the striking price before the expiration date.

As shown in the figure Vega at its highest value at 61.66 because the position contains ATM contracts. Any change in implied volatility adds change in option pricing.

Maximum Return = Unlimited

i.e. Total return = Strike Price of long put - premium paid.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Cautious about Vega on ATM Puts

Friday, May 29, 2015 7:31 AM UTC

Editor's Picks

- Market Data

Most Popular