World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

- Norway's oil & gas investments have dropped.

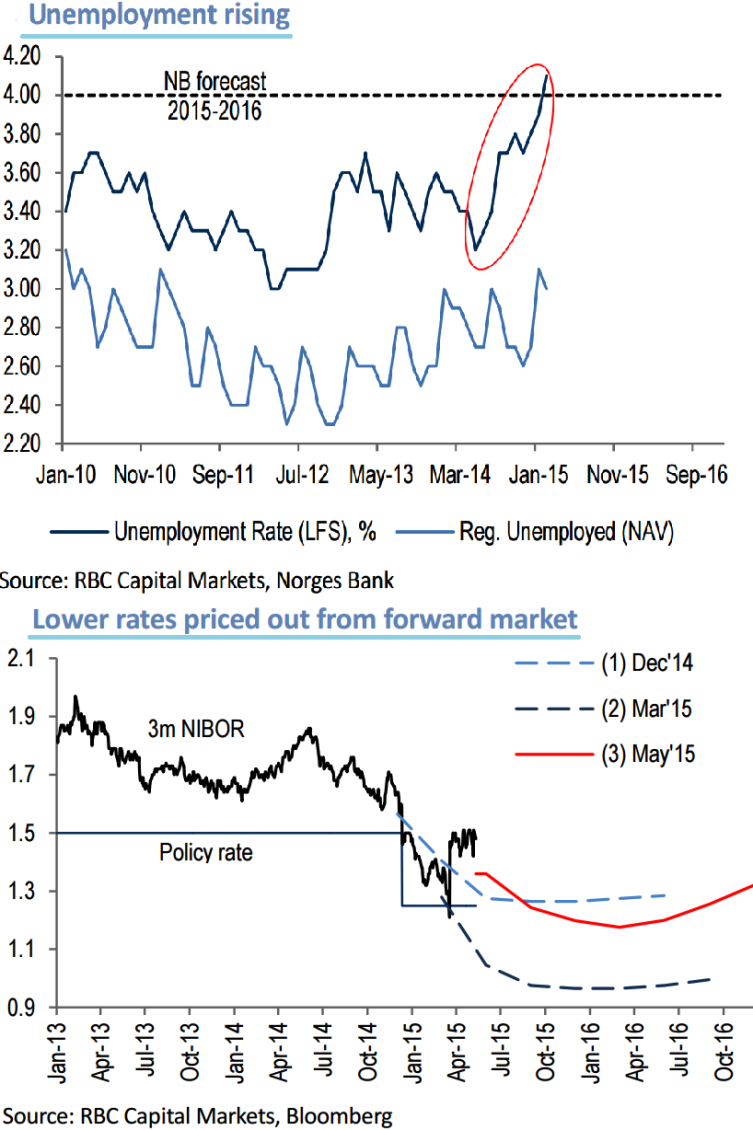

- Unemployment has increased ever since oil prices began their decline.

- GDP growth is softer but not far off trend pace.

- CPI remains close to the consensus.

- Rebound in oil prices pick up NOK.

- Lower rates priced out from forward market.

Lower interest rates and FX Forwards Advantages:

With policy rate at 1.50% last year there was plenty of room for markets to price in aggressive easing as oil prices fell from USD110/bbl to USD45/bbl.

That the Norges Bank will likely cut rates in June should see mild NOK weakness over the short term.

Past that, we suppose NOK can grind higher, with interest rates at 1.25%, NOK is a relative high-yielder in G10 that should keep the currency supported.

With the Norwegian economy proving resilient so far, as shown in the figure much of that aggressive easing has been priced out, and lifting NOK in the process. Also observe when the interests declined in April Forward volumes are spiking up.

We see in a long run EUR/NOK briefly rising to 8.70 in June on the verge of a likely rate cut by the Norges Bank. Past that, we think the pair will gradually grind lower to 8.50 by year end 2015, with a view of its extending further if oil prices continue their rebound higher.