Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300

Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

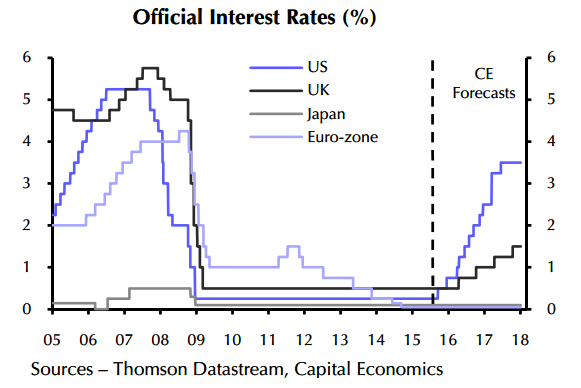

The improved US economic data means that it is almost impossible to justify keeping interest rates at near-zero. Whether the first hike is this week, or at either the October or December meetings, lift-off is surely coming soon. The first hike from the Fed since the global financial crisis will signal the end of the era of "cheap money".

The opening move is likely to be just 25 basis points (raising the target range for the Fed funds rate from 0-0.25% to 0.25-0.5%). The Fed would be likely to use the accompanying statement to emphasise that rates will rise only gradually, and only if economic and market conditions allow.

Admittedly, a number of Fed officials clearly want to use the recent volatility in financial markets as a reason to delay the first rate hike again. Some analysts do not expect the gradual return of US interest rates to more normal but still low levels to be the seismic shock that many seem to fear. The markets and most analysts now appear to expect the Fed to hold fire and many observers (including the IMF) have argued for a delay.

Raising rates now would therefore send a strong signal that the Fed is unlikely to be deflected from further tightening by additional market volatility or events overseas, unless these represented a much greater threat to the US economy. Indeed, once the dust has settled, the combination of a small hike and a relatively dovish statement may be better received than yet another delay.

"In fact, the Fed is expected to hike rates more aggressively than the markets anticipate. But the crucial point is that this is dependent on a continued improvement in the US economy, a pick up in price pressures and relative calm in the markets. If conditions deteriorated again, we would expect the Fed to pause too", says Capital Economics in a research note to its clients.

With higher US rates and a stronger USD, there is plenty of scope for looser monetary policy in other parts of the world. Monetary policy is likely to remain loose in much of the rest of the world, or even be eased further - notably in China, the euro-zone and Japan. The Bank of England might be one of the first to follow the Fed's lead, but is still likely to wait until 2016 and move much more slowly thereafter.

At 1015 GTM, the dollar was down around 0.5 percent to 119.56 yen, while the euro traded 0.13 percent lower at $1.1313, having risen to $1.1373 on Monday, its highest since Aug 26th.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Fed rate hike to give more scope for looser monetary policies in other parts of the world

Tuesday, September 15, 2015 10:52 AM UTC

Editor's Picks

- Market Data

Most Popular