BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups

Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups  Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Asian Stocks Advance as Nikkei Nears Record High Ahead of Fed Decision

Asian Stocks Advance as Nikkei Nears Record High Ahead of Fed Decision  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

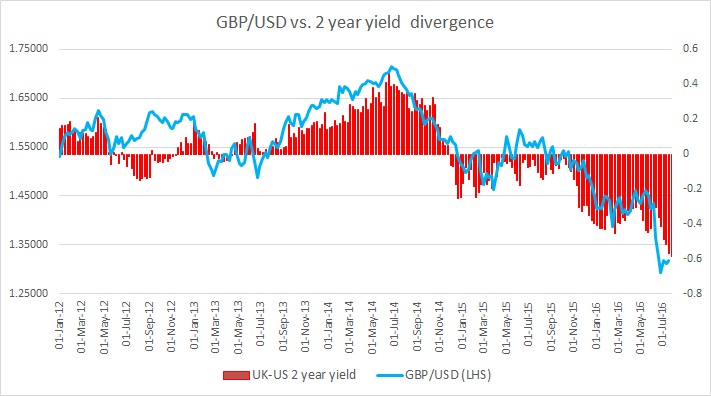

The chart above shows, how the relationship between GBP/USD and 2-year yield divergence has unfolded since 2012.

The cozy relationship between the yield spread and the exchange rate, in this case, is quite visible. Back in 2013/14, it was widely expected that UK’s economic prowess and the disappointment that the Bank of England (BoE) governor Mark Carney wasn’t as dovish as expected, fuelled the increase in yield divergence in favor of the United Kingdom and strengthening of the pound against the dollar. But as economic growth slowed and the BoE expressed a greater desire for a cautious approach, yield spread (UK-US) declined and exchange rate softened.

In 2016, the yield spread has declined sharply into the negative since the referendum date was announced. The actual decline began in September 2015 as the market was speculating that the referendum will be held in 2016, instead of 2017. The yield spread declined from -0.1 percent in September 2015 to -0.4 percent by early 2016. The spread has declined very sharply post-referendum. However, we need to note that Gilt has played the major part in this decline. Since the referendum, the yield spread has declined around 30 basis points, taking its toll on the pound.

We expect, the current high influence of yield spread is likely to continue as Bank of England (BoE) is widely expected to take some steps to ease policy further.

The yield spread is current around -0.6 percent and the pound is trading at 1.32 against the dollar.