How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market

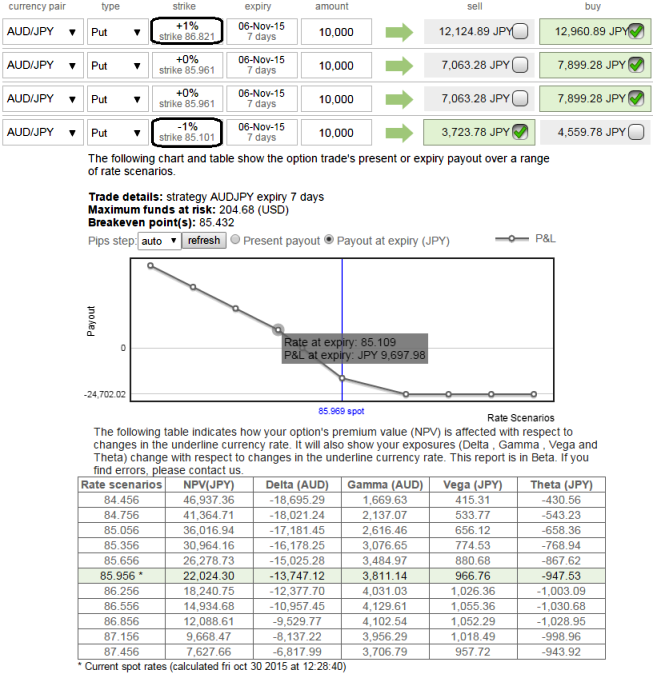

It is now BoJ's turn that keeps the policy status unchanged after Fed. The BoJ decisively has been firm by an 8 to 1 vote to leave the bank's policy target unchanged, as largely expected, indicating policymakers are confident that the economy will likely to rebound in the near future.

So far we all know that the position uses long and short puts in the ratio of 2:1, now alter it into 3:2 so as to maximize the returns as we could sense the more downside potential but again it depends upon risk appetite and returns expectations.

The implied volatility of 1M ATM AUDJPY put contract has nothing much changed, it is almost close to 14% which is quite on higher side that is good sign for option writers.

We know that the options with a higher IV cost more, intuitively due to the higher likelihood of the market 'swinging' in your favour. If IV increases and you are holding an option, this is good. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

Hence, as shown in the diagram weights have been doubled and resulted into huge cash inflows for every small change in underlying exchange rate.

As we expect the underlying currency exchange rate of AUDJPY to make a larger move on the downside. As shown in the figure purchase 2 lots of At-The-Money -0.52 delta puts, 1 lot of OTM put and simultaneously short 1W 2 lots of (1%) In-The-Money put option.

Entering into this AUDJPY position which has higher implied volatility at 14% and expecting for the inevitable adjustment is a smart approach, regardless of the direction of price movement.

Based on volatility and time decay, the strategy is a "price neutral" approach to options, and one that makes a lot of sense.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: AUD/JPY ATM IV still favors put writers – 3:2 PRBS to extract max leverage

Friday, October 30, 2015 7:30 AM UTC

Editor's Picks

- Market Data

Most Popular