How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

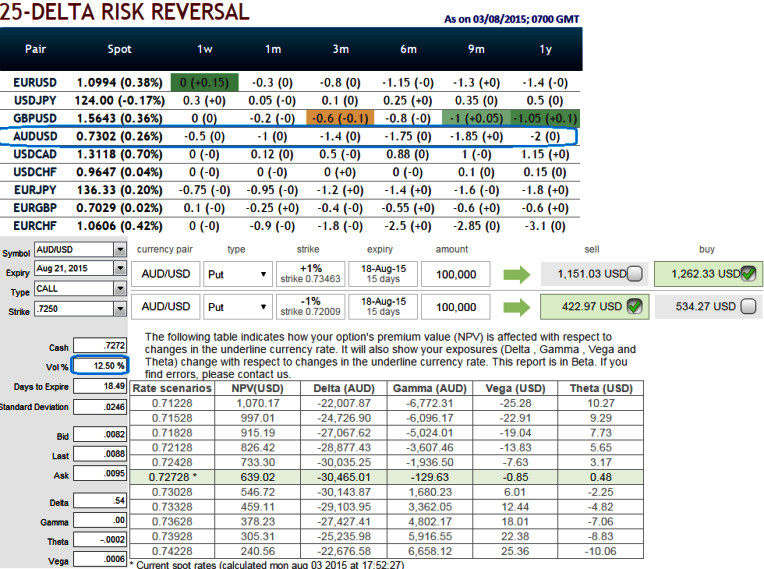

Rationale: Prevailing implied volatility rates for AUD/USD ATM 1M-6M contracts are in range of 12% to 14%. But higher negative delta risk reversal indicates put contracts have been relatively costlier. In the nutshell, AUD/USD Out of the money options are trading with negative delta risk reversal which would mean that downside risk protection is more expensive.

The downside risk in AUD against USD is anticipated as the Fed's rate decision seems to be is in line with the Yellen's hints after she sent strong indications that US economic conditions are likely to justify an interest rate hike at some point this year. But Aussie import prices QoQ are improved by 1.4% which is in line with forecasts.

For Australian exporters who have their receivable exposures in AUD, we advocate gamma spreads rather than naked puts (even OTM puts have been expensive). As the risk appetite varies from different investors to different traders, we've customized our formulation of strategies for such varied circumstances.

When the above naked put option was highly sensitive to the underlying exchange rate of AUD/USD, we think it adds to the risk and reward profile for both options holders and writers. So, buy 15D (1%) In-The-Money 0.15 gamma put option and short 15D (-1%) Out-Of-The-Money put option for net debit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: AUD/USD delta risk-reversal signifies overpriced puts; HY gamma spreads for IV riddle

Monday, August 3, 2015 12:30 PM UTC

Editor's Picks

- Market Data

Most Popular