Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

The Australian federal government’s mid-year fiscal update is expected to show a deteriorating deficit as broad economic weakness offsets commodity price gains. Markets will be watching for any rating agency reactions. The Aussie crosses remain edgy, especially pairs like AUDNZD, AUDJPY well below fair value estimates implied by interest rates, commodity prices, and risk sentiment. However, Australia’s AAA downgrade risk is to be acknowledged, any such action likely to delay any return towards fair value during the next few month.

It seems rational that antipodeans currency crosses as “high yielding” avenues that suffer more as a result of the USD strength than most other G10 currencies.

From that point of view, it seems illogical that the yen is also suffering disproportionately. It seems that the new BoJ strategy that was only received moderately positively before the election, is now perceived to be much stronger in the form of Fed’s delivery of rate hike.

The fact that the BoJ is fixing long-term JGB yields seems a much more important measure if US yields are rocketing as a result of the new Fed view.

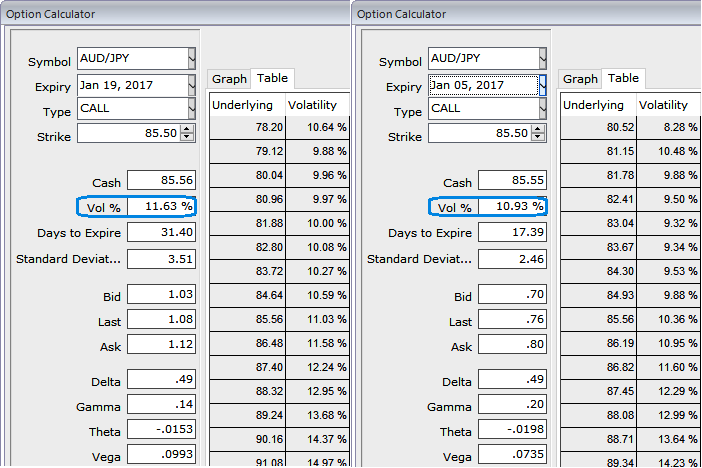

BoJ’s monetary is policy is scheduled for tomorrow, for this week, we think the pairs such as AUDJPY are blowing IVs crazily in OTC FX space that pops up with rising IVs above 10.93% for 2 week expiries and 11.63% for 1m tenors having significance in economic drivers that propels this currency pair to anywhere.

We retain our outlook for the BoJ to stand pat until at least mid-2017 when we expect the effects of fiscal stimulus to start fading. Next week’s focus will likely be on the post-MPM press conference and any comments BoJ Governor Kuroda may have about how yield curve control will be implemented amid rising yields

We think the same HY IVs with longer tenors are conducive and justifiable for option holders as there are series of considerable economic events lined up going forward.

Well, in order to arrest this upside risk that is lingering in intermediate trend and prevailing declining trend, we recommend diagonal option strap strategy that favors underlying spot’s upside bias in long run and mitigates bearish risks in short term.

So, we recommend building the FX portfolio exposed to this pair with longs positions in 2 lots of 1M ATM 0.51 delta calls and 1 lot of ATM -0.49 delta puts of 2w expiries.

Since, the slumps are likely in near term and upswings in near term seem to be dubious as per the signals generated by technicals as well as from IV skews, AUDJPY option straps strategy should take care of both upswings and downswings simultaneously, even if BoJ surprises with the forecasters and the strategy is likely to derive handsome returns on the upside and certain yields regardless of swings on either side but with more potential on upside.