Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

The combination of the OPEC deal and the prospect of cuts by non-OPEC producers was a better-than-expected outcome for oil and our commodity strategists stay bullish, looking for Brent to reach $60/bbl in December 2017.

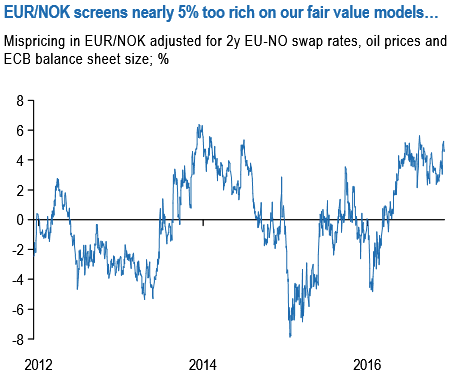

Within G10, NOK stands out as an attractive candidate as it still appears cheap relative to rate differentials and oil prices (refer above chart).

Moreover, the central bank is expected to hold policy steady as growth appears to have bottomed and the balance of payments dynamic remains supportive. Admittedly inflation missed expectations this past week, but we continue to think that growth matters more for the Norges Bank, the outlook for which is better with higher oil prices.

On the other hand, CAD stands out as a candidate to short as it will be vulnerable if a hard line on trade emerges from the US (particularly around NAFTA). Hardly any concession is priced into CAD for any such political risk and Canada’s external position remains vulnerable with current account and basic balances both in deficit territory.

Moreover, in the latest meeting, the BoC continued to be focused on disappointing business investments and nonenergy goods exports, while also hinting at a period of diverging monetary policy between the US and Canada (Bank of Canada remains on hold as widely expected).

The combination of virtually no political risk priced in to CAD, combined with cheap NOK valuations had prompted us to initiate long NOK vs. CAD. The trade also had a soft exposure to long oil prices pre-OPEC.

We further increase our long oil exposure via NOK, recommending the longs vs. EUR. Increase long exposure to oil; buy NOK vs. EUR outright to prior long NOK vs. CAD.

Hence, the outright trades read this way,

Stay short in EURNOK via vanilla option structures, 2m ATM delta put options at spot reference 9.0530.

Short CADNOK at 6.4938 with a stop at 6.5725. Marked at -1.55%.