US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

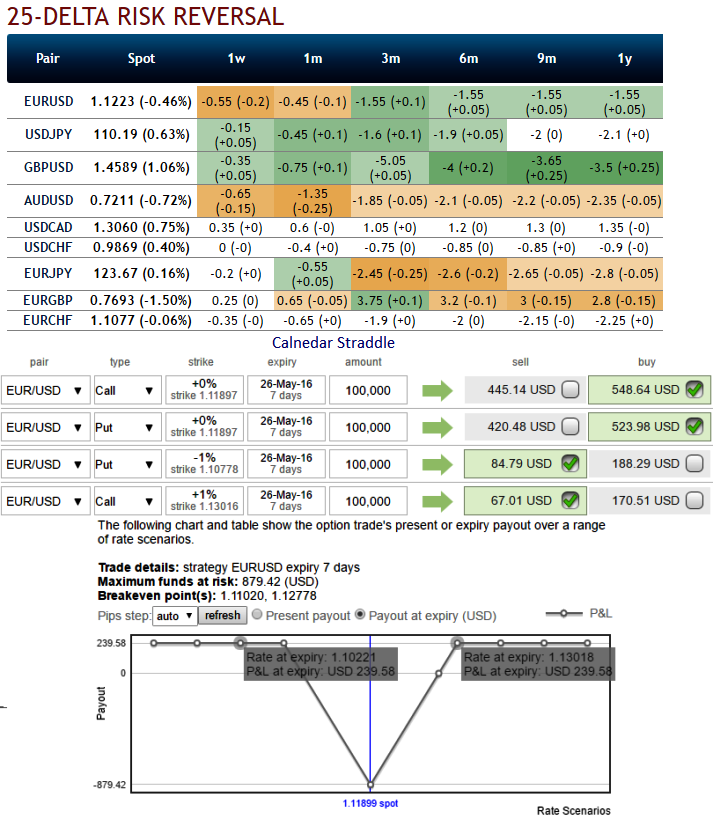

Bounce in realised volatility is most likely upon event risks as stated in our recent write up volatility regimes.

Please go through below link for more reading on EURUSD IVs:

Risk reversals also divulge the more activities in FX OTC markets with positive tickers especially during in 3m tenors which would substantiate IV shifts that is stated in above write up.

Ever since we first saw a rise in the hawkish comments on the part of FOMC members from the start of the month, the US currency has been appreciating by approx. 2.8% against the other G10 currencies (adjusted by risk-off effects) as well as IVs in this dollar crosses.

At spot ref: 1.1187, go short in 2W (1%) out of the money calls + short in 2W (1%) out of the money put options with lower positive thetas or closer zero.

Simultaneously, go long in 2M at the money with 50% delta and long in at the money put option with same tenor and 50% deltas.

Maximum gain for the strategy is earned when the EURUSD is trading at the strike price of the options sold on expiration of the near term straddle.

At this price, both the written options expire worthless while the longer term straddle being held will suffer only a small loss due to time decay. Thereafter, underlying spot FX has to show more move on either direction.

The maximum profit is limited to the extent of only on or before expiry of the near term straddle as the options trader has the option of holding on to the longer term straddle to switch to the long straddle strategy which has unlimited profit potential.

Pease be noted that the tenors shown in the diagram are for demonstration purpose only, use accurate tenor as stated above.