Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

Speculations about early rate cuts in Mexico are increasing: As price data published yesterday showed, inflation continues to decline. In early July it fell to the lowest level in the past two years. That puts inflation at the upper end of the range but within the Banxico's inflation target of 2-4%.

At the same time, growth leaves much to be desired: Seasonally adjusted GDP shrank by 0.2% in the first quarter of 2019, and the second quarter should not have been too excitingly either - the preliminary GDP data scheduled for next week will provide more clarity in this respect.

In view of the gloomy growth outlook, forecasts for the current year are being lowered in many places: This week, the IMF revised its - admittedly so far quite optimistic - outlook and now expects a growth rate of 0.9%, just as we do.

All in all, good inflation data and weak growth numbers increase the chance that Banxico will start lowering key rates by the end of the year as we expect. For the MXN, this will probably mean somewhat weaker levels in the future.

We, therefore, do not reckon the current levels sliding below 18.75 in USDMXN to be sustainable, while the major uptrend remains robust.

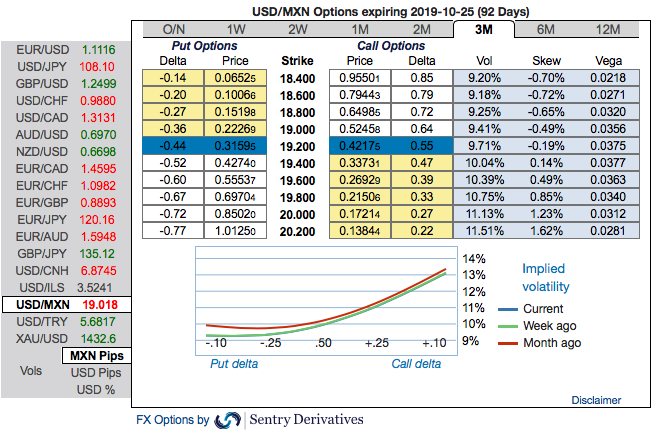

OTC updates: Of late, MXN seemed to be extending recovery threatening upper bound of the recent range. Please be noted that the 3m USDMXN implied volatility skews signal continued upside risks, bids for OTM call strikes up to 20.20 levels. The previous massive sell-off of Mexican peso caused a vol surface dislocation, nudging skews to the highest since the 2016 US Presidential elections. Delta hedged 1*1.5 ratio call spreads exploit the dislocation while also having historically offered a superb performance. +1Y/-3M calendars of risk reversals take advantage of the lagging back-end vs front-end implied skews. Courtesy: Commerzbank & Sentry