Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

How much further will the Brazilian central bank (BCB) cut its key rate? Today it will certainly cut it by a further 50bp to then 5%. It had signalled its willingness to do so at its last meeting in September, and the conditions for further easing are given. In September inflation stood at 2.9%, i.e. at the lower end of the BCB’s target corridor (2.75 - 5.75%). Moreover following a long-winded process the much feted pensions reform was finally passed by the Senate as well last week. As a result a major factor for uncertainty, which the BCB had also constantly referred to, has been overcome and as a consequence BRL was able to appreciate over the past days.

In addition, with the major domestic political risk out of the way after the passage of the social security reform in Brazil, and the global environment expected to be relatively benign over the next few weeks, there is room for BRL vols to catch-down to the softening in the rest of the EM vol complex over the past two weeks.

We do not expect BRL to be disrupted either by proxy hedging demand in the run-up to the upcoming Argentina election, or by the postponement of the December oil auction. 1M ATM vol (12.8) is already 1 pt. lower from its local high, and we reckon that realized vol can soften to below 10% with the SSR out of the way.

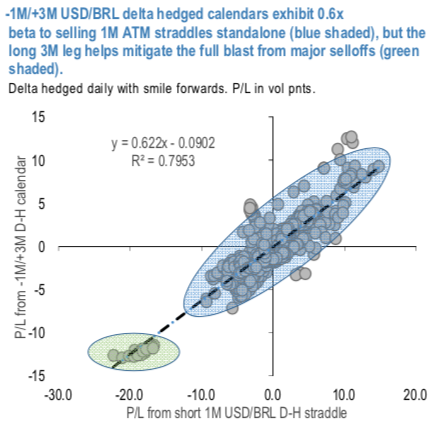

Given the flatness of the front-end of the vol curve (3M – 1M spread 0.2), we consider it prudent to quasi-hedge the outright gamma short by structuring it as a -1M / +3M straddle calendar (vega-neutral, delta-hedged).

The above chart shows that such calendar spreads capture 0.6x of the returns of standalone short 1M delta-hedged straddles on average, but the long 3M leg helps partially shield the structure from full impact of major vol shocks. Alternatively for maintenance free exposure consider 1M USDBRL vol swap @12ch vs. 1M1M FVA @12.55/13.1 indic spread, in equal vega.

Sell 1M @12.4 ch vs. buy 3M USDBRL delta-hedged straddles @12.5/12.85, vega-neutral, as a quasi-hedged outright gamma short. Courtesy: JPM