Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

The Federal Open Market Committee starts its next two-day policy meeting on March 14. US Non-farm Payrolls' solid reading on Friday reinforced market expectations of Fed rate hike in March. February jobs report removed the last obstacle for a Fed hike on Wednesday, in line with the message Fed Chair Yellen set in her recent speech.

Friday’s reading from non-farm Payrolls showed the economy added 235K jobs during February, although wage inflation slowed its pace. The unemployment rate edged down to 4.7 percent in February from 4.8 percent in January, in line with expectations. The report also said the annual rate of growth in average hourly employee earnings accelerated to 2.8 percent in February from 2.6 percent in January.

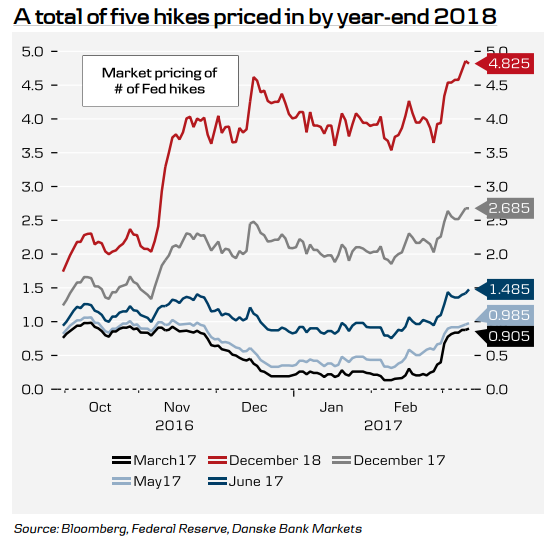

Markets have fully priced in an U.S. interest rate rise when the Federal Reserve meets this Wednesday, a view cemented by robust U.S. jobs data. Markets are also now more aggressive for the rest of the year, moving closer in line with the 'dot plot' indication of three hikes.

A Bloomberg survey of 45 economists conducted on March 7-8 showed three 25bps rate hikes by the Fed in 2017, with moves expected in March, June and December. Previous survey had revealed expectations for 2 hikes this year. The survey also showed economists lifting their average projections for the fed funds rate at the end of 2018 and 2019 by a quarter point, bringing those in line with Fed expectations as well.

Minutes from the previous Fed meetings revealed that FOMC members have become more vocal on their desire to reduce the Fed’s balance sheet in recent months. The Fed wants to begin the reduction when the normalization of the Fed funds rate is ‘well under way’, which seems to be when it is around 1.50 percent. Analysts feel the Fed will soon begin to discuss ‘the economic conditions that could warrant changes’ in the current reinvestment strategy ‘at upcoming meetings’.

"We expect the Fed to hike three times this year (March, July and December). We think the Fed will begin the reduction in Q1 18. An NY Fed survey shows that primary dealers expect it to begin a bit later in mid-2018," said Danske Bank in a report.

The U.S. Treasuries recovered Monday as investors covered previous short positions after reading upbeat labor market report on Friday. The yield on the benchmark 10-year Treasury fell 1 basis point to 2.57 percent, the super-long 30-year bond yield slipped 1-1/2 basis points to 3.15 percent and the yield on short-term 2-year note traded nearly 1 basis point lower at 1.35 percent by 1140 GMT.

EUR/USD was trading largely unchanged at 1.0674 at around 1230 GMT after hitting highs of 1.0714. USD/JPY was trading in a narrow range on the day, currently at 114.66. FxWirePro's Hourly Dollar Strength Index remained neutral at -49.8952 (a reading above +75 indicates a bullish trend, while that below -75 a bearish trend). For more details, visit http://www.fxwirepro.com/currencyindex.