Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

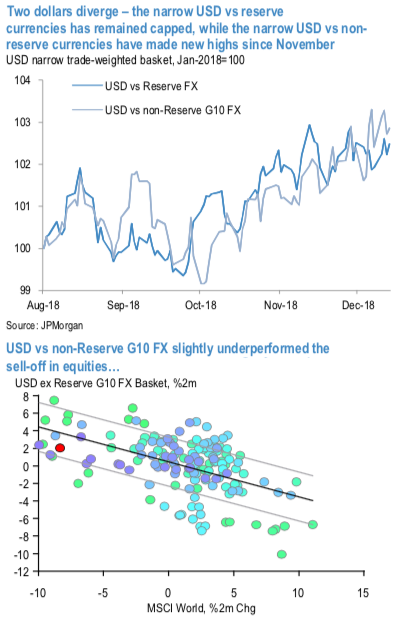

Since late November, as the US cycle risk repricing was unfolding, the dollar went on to make new highs versus its narrow non-reserve FX basket, while narrower US rate spreads helped contain USD strength versus other reserve currency peers (refer 1stchart). From this “two narrow dollars” perspective, the dollar has modestly undershot non-reserve G10 currencies (by 1.7%) given the magnitude of sell-off of global equities (refer 2ndchart). But the USD has remained unusually resilient against other reserve currencies given the narrowing of rate spreads, staying flat rather than declining 1% as a hybrid rate/yield curve spread model might suggest.

EURCHF is a realistic proxy for a tactical short in EURUSD given that the two has been 85% correlated over the past three years. Whereas we suspect this relationship is at risk of breaking down should EURUSD ever rally aggressively, we suspect EURCHF will continue to closely track EURUSD whenever the euro is under pressure. This all comes down to Switzerland’s superlative external position and the possibility that the SNB has reached or is closer to the limits of its ability to intervene to frustrate a fundamentally justified appreciation in CHF.

Simply put, the SNB has recycled virtually all of Switzerland’s current account surplus for a decade (contrast this with the BoJ which has done none), yet the SNB’s ability maintain this policy in a shakier asset market environment is questionable with the balance sheet at 122% of GDP and provisions sufficient to cover only a 17% asset write-down (i.e. the SNB is effectively 5.3x levered). The SNB has notably omitted to intervene since the spring despite the Italian crisis and it can be no surprise therefore that the CHF NEER is 6% higher than the trough in May.

When we published the 2019 Outlook we argued that the big dollar turn was not yet imminent. Nevertheless, the base case for 2019 does envisage a handover from US to Euro area growth and mean-reversion in undervalued European FX. SEK screens as the cheapest European currency (REER 14% below 20Y average) and also has a central bank that is poised to slowly reverse its multi-year experiment with super easy monetary policy. We consequently added a medium-term put spread in USDSEK, but structured it as a 1-1.5x to lower the cost as we lacked conviction that the trade was yet poised to work. We weren’t wrong in that judgement; it obviously remains to be seen whether EUR and SEK can turn things around against the dollar by the middle of 2019. Courtesy: JPM

Trade tips:

Sell EURCHF at 1.1244 with a stop at 1.1469.

Long a 6M 8.55-8.15 USDSEK ratio put spread in 1x1.5 notional. Paid 76bp. Marked at 46bp.

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards 27 levels (which is mildly bullish), while hourly USD spot index was at 78 (bullish) and CHF is at 0 (absolutely neutral), while articulating (at 10:19 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex