Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

The massive dollar uptrend is peaking with the massive repricing of yields triggered by the December Fed meeting. The FX space is now in consolidation mode, and the recent FOMC minutes were either neutral or slightly hawkish but delivered nothing that justifies lower real yields. All in all, USD directional positions are currently less appealing, and we look thus for opportunities in the crosses space, where EURJPY stands out with little bullish potential in short run.

But Euro area political and US policy risks will be the immediate drivers of the euro. In the Euro area, our base case continues to be that traditional parties will prevail (The euro in 2017: Populism precedes an ECB policy shift). Immediate focus will be on the Dutch general elections (March 15th) and polls for the French elections (April-May). Given the uncertainty around US policy, positioning for Euro area political risks is better expressed through short EUR/CHF rather than EUR/USD.

On the other hand, we expect foreign investors, who have sold JPY aggressively since the US election, to be possible buyer of JPY again, hence, expect strength in Yen. But the major headwind is that the BoJ’s meet on January 30-31. While we expect inaction of the BoJ until Kuroda’s term ends in April 2018, Outlook Report will garner attention at the upcoming meeting.

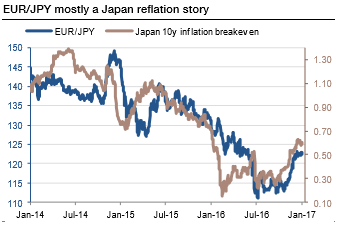

EURJPY has essentially traded as a function of the Japan reflation story (refer above graph) since the start of 2014. Interestingly, large EURJPY variations have been well anticipated by the gyrations in Japan 10y breakevens.

They bottomed at 0.2-0.3% in 2016 but have recovered to 0.6%. The BoJ certainly expects to continue to do its best to engineer a more ambitious repricing in inflation expectations (expect it to again use the quantitative toolkit).

As EURJPY trends are well explained by a Japanese factor, one may presume that they have been quite insulated from euro moves. But reflation has had a major impact on both EURUSD and USDJPY. This is not totally coincident, and the euro remains a factor.

While there is likely still euro downside to come, the pace is now likely to slow, as the market should remain reluctant to reinstate massive EURUSD shorts below 1.04 in a context of euro area inflation surprising on the upside this week.