RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Market participants have been on the edge leading into the last policy meeting of the US FOMC, with the VIX spiking to over 25 this week (first time since early February 2018). In the event, the Fed sounded only marginally more cautious, with its members guiding expectations of two further policy rate hikes next year on top of the 25bps hike from today. This may not please the markets, but we find today’s decision and the guidance quite reasonable. Many analysts shade their forecasts to two rather than three FOMC hikes next year, however, emphasis on essentially back to data dependency i.e. if wage inflation accelerates further amid still resilient growth, there is little to stop the FOMC from doing a third hike if the data warrants it. While the FOMC has acknowledged market concerns about a slowing US economy and trimmed its median expectations from three to two hikes next year, the FOMC statement and refreshed economic forecasts.

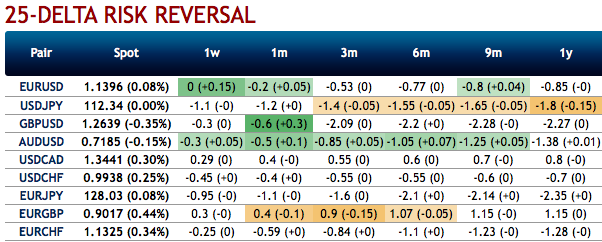

OTC indications: Above aspects are factored-in OTC markets, while the bearish standpoint is turned on USD vols following their intraweek spike. It is difficult to discern an overarching macro theme from the messy and differentiated price action of the past week.

Negative risk reversal numbers of all dollar pairs are also substantiating the downside risks. Note that fresh negative bids are observed for almost all USD crosses, for an instance, please also be noted that IVs of USDJPY that display are tepid among entire G10 FX universe.

While the positively skewed IVs of 2m tenors signify the hedgers’ interests to bid OTM put strikes (refer above nutshells evidencing IV skews).

Trade tips: We feel quite fortunate to be exiting in the black having owned USDJPY through a deep and sometimes volatile correction in US stocks. This wasn’t entirely happenstance - we have argued that structural capital outflows from Japan together with super-wide front-end differentials would dull the yen’s immediate sensitivity to certain falls in risk markets. But we don’t want to stick around too long to find out where the pain threshold for Japanese investors might actually be - we assume that even corporates will slow their accumulation of foreign assets in response to a sufficiently adverse set of macro or market conditions.

USDJPY trade should be squared-off marked at 0.56%, that were bought in September.

Alternatively, on hedging grounds, we advocate shorting USDJPY futures contracts of mid-month tenors as the underlying spot likely to target southwards in the medium-run. Writers in a futures contract are expected to maintain margins in order to open and maintain a short futures position.

Currency Strength Index: FxWirePro's hourly USD spot index was at -52 (which is bearish), while hourly JPY spot index was at 82 (bullish) at 08:04 GMT.

For more details on FxWirePro's Currency Strength Index, visit: http://www.fxwirepro.com/currencyindex