Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

CAD risk skewing positive, as BoC dovish stance bending, though not yet breaking:

Ongoing data surprises mean forecast upgrades forthcoming in next week’s Monetary Policy Report. The data flow from Canada, similar to what has been seen globally, has surprised almost persistently since last September (refer above diagram). Our economists have raised their own 1Q GDP growth forecast to 3.8% and have penciled a first BoC’s hike in 3Q18. BoC will likely have to make similar upside revision both global and its own Canada forecasts –the January MPR it estimated 4Q16 and 1Q17 at 1.6% and 1.5%yoy respectively compared to an actual 2% in 4Q and a January 2.3% print (refer above diagram). Meanwhile, BoC's 1Q17 projection for headline inflation was 1.8% versus actual inflation in first two months of the year which averaged 2.0%.

But this is unlikely to shift BoC away from its dovish stance. This begs the question whether the forthcoming forecast upgrades will shift the BoC stance in a meaningful way for CAD; we think unlikely, in the near-term at least. First, is simply the stubborn dovish persistent rhetoric over the past month from BoC Gov Poloz and other senior officials, as recently as last week downplaying the strength of recent headline data, emphasizing still-sizable excess capacity, downside risks, and warning against expectations that BoC would mirror the Fed in the US’s policy normalization cycle.

Below the surface of the headline data, BoC’s dovish stance still has solid legs to stand on. The view of ongoing slack is reinforced by ongoing weakness in both core inflation numbers -which has been persistently running round 0.4%-pts below the 2% target, as well as trend-weakening seen in wage data, inclusive of today’s payrolls report showing the slowest average hourly earnings growth on record. Moreover, the foundation of BoC’s unusually cautious view is an observation that the non-commodity export sector is suffering from competitiveness issues from an incomplete rebalancing.

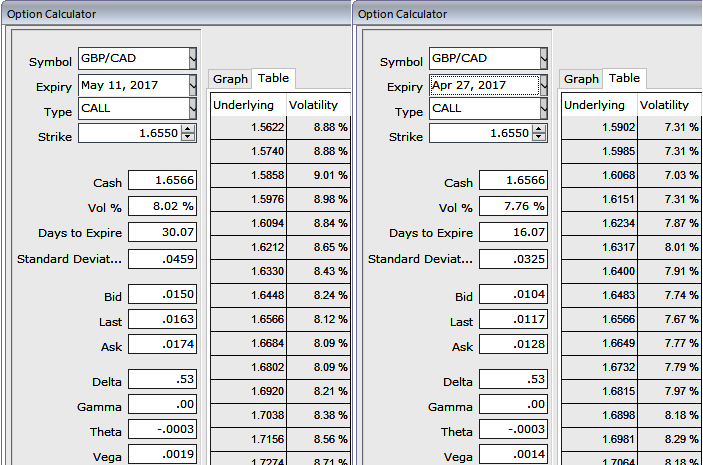

OTC updates and hedging framework:

The main reason behind this decision is that the BoE would not want to add any extra strain on the markets and the British economy in conjunction with the Brexit apprehensions by allowing any speculation about an adjustment of its monetary policy.

Please note that in OTC markets, the IVs of this pair is just shy above 8% and a tad below 7.8% for 1m and 2w tenors respectively.

These ATM IVs seem to be quite on the edge to factor in the weakness in this pair as we could see the reasonable increase in IVs of 2W and 1M tenors. As a result, we recommend capitalizing on the sustainable IV factor by employing ITM short puts as their central bank's decision was also in line with market's expectations and matching this with ATM longs to construct short-term back spreads that is likely to fetch positive cash flows as per the indications by sensitivity table.

When trying to assess how a spread may perform, looking at the 2m IV skews spreads of out of the money option shorts for an indication of relative option prices seem attractive.

So, keeping all these attributes in mind here goes the strategy, go long in 1M 2 lots of ATM -0.50 delta put, and in 2M (1%) OTM -0.36 delta puts while shorting 1 lot of ITM put (0.5%) put with 2-week expiries.

Subsequently, the slight upward or sideway swings would derive the positive cashflows through the initial receipts of shorts which could be utilized for reducing hedging cost.