Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears

Asian Stocks Rise as Weak US Jobs Data Eases Fed Rate Hike Fears  China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases

China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  Oil Prices Rise as Hormuz Reopening Remains Uncertain

Oil Prices Rise as Hormuz Reopening Remains Uncertain  US Dollar Near Two-Month Low as Markets Await Inflation Data

US Dollar Near Two-Month Low as Markets Await Inflation Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

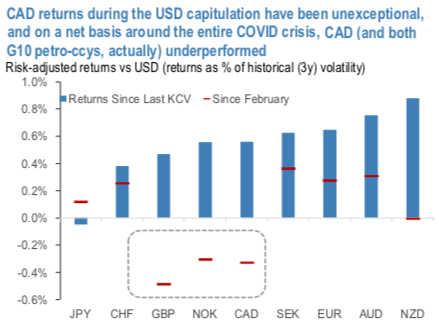

USDCAD has fallen a sizable 4% since our last publication, but this is reflective entirely of the broad dollar’s anti-cyclical properties and negative beta to risk, and is not indicative of outright CAD outperformance. CAD headwinds bias our USDCAD forecasts higher over the medium-term. In some ways, that CAD has only depreciated 2.2% on net against the dollar since March despite the intervening pandemic-led global recession, Saudi-Russo price war, briefly-negative oil prices, and the single greatest Canadian economic & labor market shock ever is remarkable. But this is indicative more of the recent market paradigm shift around risky markets and the USD which has whole-heartedly embraced of the reopening of global economies and the attendant bounce-back in growth, despite the fact that global benchmark oil levels are still 25-30% below pre-crisis levels and US & Canadian unemployment could remain above 10% of the remainder of the year. Indeed, despite USDCAD touching 1.33 and dropping 6.5% total since mid-March, CAD is unexceptional when compared against other G10 currencies this month and, against pre-COVID levels, CAD is actually a relative laggard in G10 (refer above chart).

Thus, despite recent USDCAD weakness, we continue to harbor reservations about the prospects of CAD’s resilience this year, but believe this pessimism is better expressed tactically through crosses than versus the USD as the latter continues to consolidate in the pro-growth environment and as CAD remains well-correlated with riskier assets.

Trading tips: At spot reference: 1.3653 levels (while articulating), one-touch call options strategy is advocated using upper strikes at 1.38 levels. One can see exponential yields as the underlying spot FX keeps spiking towards upper strike on the expiration.

Alternatively, we recommended directional hedges that comprised of longs in USDCAD futures contracts of July’20 delivery, simultaneously, shorts in futures of June’20 delivery. The short leg has delivered desirable hedging objectives so far due to the price dips in the recent past. While long leg of July tenor should be upheld with an objective of arresting potential bullish risks.