2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise

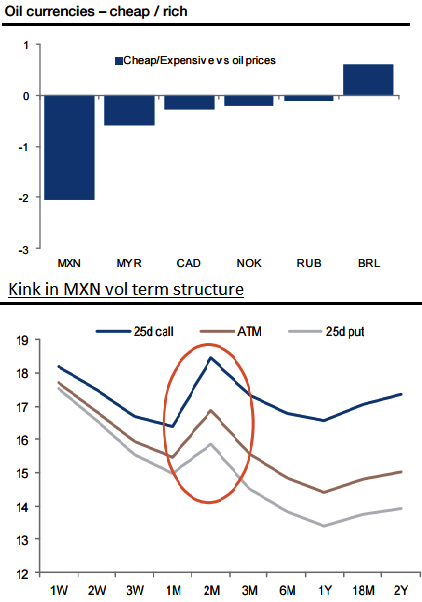

The MXN is around two standard deviations cheap versus oil prices as you can observe in the above chart (based on a weekly regression of FX and oil prices since 2014), while the rest of G10 and EM oil-driven currencies are within 0.5 standard deviations.

The risk premium in the MXN seems related to US politics, and specifically a non-negligible chance that Trump wins in November. Risk premium is not discernible in other currencies or asset classes.

Given the potential sensitivity of the MXN to a Trump victory, the term premium is most noticeable in USD calls. By comparison, the risk premium around the US election is non-existent in other EM currencies.

Selling MXN vol and buying vol in other EM currencies that might come under pressure (KRW, TWD, and TRY) might be worthwhile to consider.

In US election: impact on currency markets we analyse five transmission channels to build an EMFX Trump-vulnerability index.

There is a distinct kink in the MXN vol term structure between the 1m and 3m tenors that straddles the US election (November 8).

EM currencies fear Trump. The ZAR, MXN and MYR have been most sensitive to improvements in Donald Trump’s poll results.

Hence, short AUDMXN to fade US political risk premium and capture MXN being cheap vs. oil and AUD expensive vs. rate differentials (link).