Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

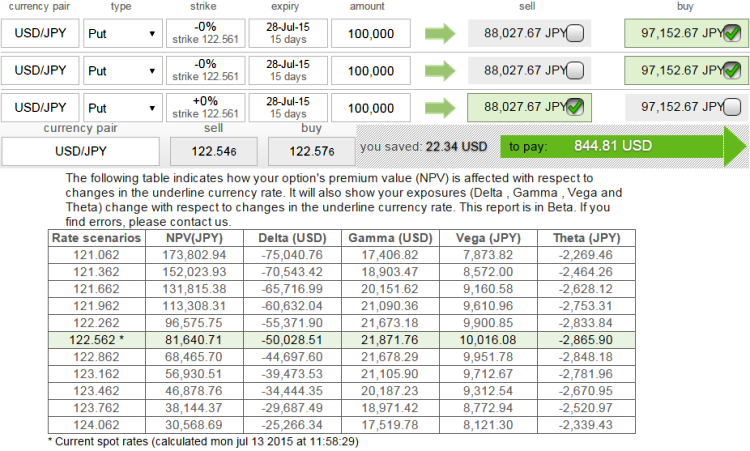

Arrest short-medium term downside risks of USDJPY hedging through deploying option strategy: Put Ratio Back Spread

Is the US growth forecast downgrade now complete? We are optimistic that it is and that the drag on the dollar from growth forecast downgrades is behind us. With fed funds futures priced for a 0.9% rate in Q4 16 and a 0.25% rate in Q4 15, we don't envisage much more downward revision to rate expectations. That helps the dollar though won't be a major factor unless or until the US rate forecasts start shifting in the other direction.

Expect the underlying currency cross (USDJPY in this case) to make a reasonable move on the downside in medium terms.

For short term hedgers the recommendation would be; Purchase (1%) OTM puts and sell fewer puts of a higher strike (ATM or ITM) usually in a ratio of 2:1, 3:2 or 3:2.

This is more attractive strategy, basically, as you're selling an at-the-money short put spread in order to help pay for the extra out-of-the-money long put.

The higher strike short puts finances the purchase of the greater number of long puts and the position is entered for no cost or a net credit.

Keep an adequate time for maturity so as to make a substantial move on the downside.

Delta prices and measures options strategy correctly: As shown in the figure it is observed that this strategy offers reliable delta (-50028.51) at prevailing exchange rate which means we are short on USDJPY in underlying market. So, we are participating in Yen as long as it holds its strength but when USD gains appreciation, delta responds proportionately (-25266.34) which means our shorts in underlying have reduced and we are also participating on upswings as well.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Optimism seen on dollar growth forecasts but delta assures optimal pricing of USDJPY PRBS

Monday, July 13, 2015 6:43 AM UTC

Editor's Picks

- Market Data

Most Popular